2026-07-20

MayRetire is a retirement planning application for Canadians. It helps you model retirement cash flow, withdrawals, taxes, portfolio evolution, and estate outcomes for single or couple plans.

This draft reflects the latest sections documented from current app screens and source behavior.

? icons for contextual help on fields and

panels.+ / - controls or type values

directly.

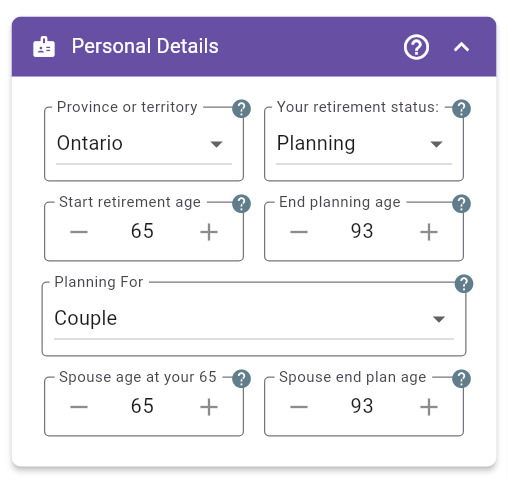

Figure 1: Personal Details - Planning

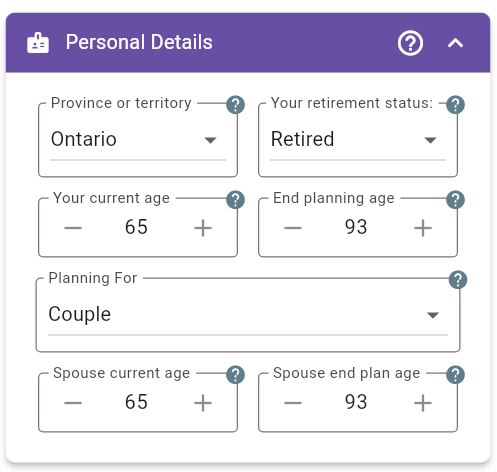

Figure 2: Personal Details - Retired

This panel establishes the timeline and household context for the entire model. Age inputs here affect pension start logic, tax modeling, survivorship projections, and how many years your assets must support spending.

Province or territory Select your current province or territory of residence. MayRetire applies province-specific tax brackets and credits to all annual calculations.

Your retirement status (Planning or

Retired) Use Planning when retirement

has not started yet. Use Retired when it has already

started. This switch changes several fields from projected values to

current values so the model starts from the right baseline.

Start retirement age (Planning mode) The age at which retirement cash-flow modeling begins.

Your current age (Retired mode) Your age at current year-end. This helps MayRetire position your plan correctly on the timeline and apply age-triggered rules immediately.

End planning age The final age in the projection horizon. A longer horizon usually lowers apparent plan safety unless assets/spending assumptions are adjusted.

Planning For (Single or

Couple) Chooses one-person or two-person household

planning. Couple mode enables spouse timelines and tax-sharing logic

used throughout the plan.

Spouse age at your retirement age (Planning + Couple) Spouse age in the year your retirement starts. This aligns partner timelines correctly for benefits and tax treatment.

Spouse current age (Retired + Couple) Spouse age at current year-end for in-retirement couple modeling.

Spouse end plan age (Couple) Final projection age for spouse. Important for longevity and survivor-risk analysis.

Practical guidance:

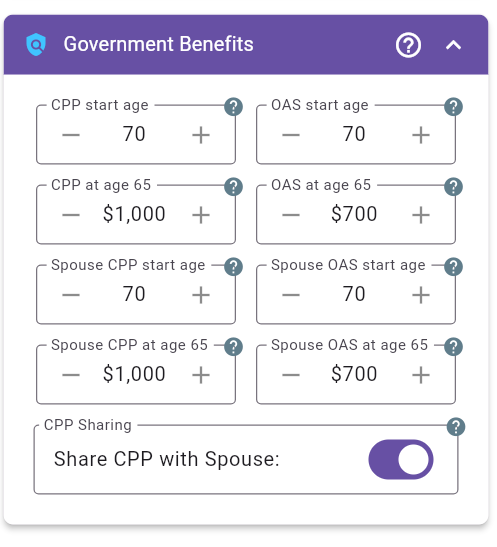

Figure 3: Government Benefits - Planning

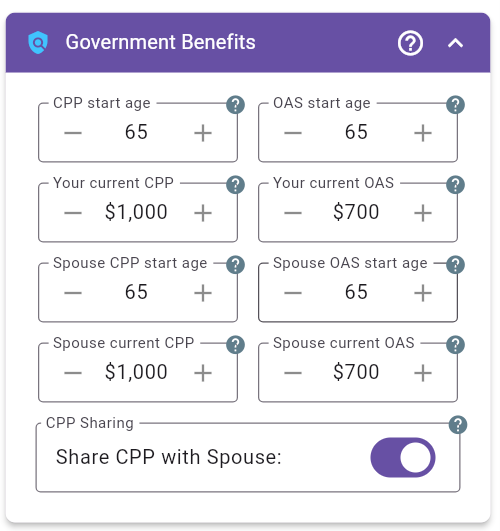

Figure 4: Government Benefits - Retired (CPP/OAS started)

This panel configures guaranteed government income from CPP/QPP and OAS for both partners (if applicable). These settings strongly influence required withdrawals, taxes, and long-run sustainability.

In couple mode, the left column is for you and the right column is for your spouse, with matching benefit fields aligned on the same row. In single mode, each applicable field expands to the full panel width.

CPP start age Choose the age CPP/QPP starts (typically 60 to 70). Starting earlier reduces monthly income; delaying increases monthly income.

OAS start age Choose OAS start age (typically 65 to 70). Deferral increases monthly OAS.

CPP amount (Planning-style input) Enter

your projected monthly CPP/QPP amount and then choose

Estimation at: 65 | 70 | Start. Use 65 if the

amount is your estimated monthly CPP at age 65. Use 70 if

the amount is your estimated monthly CPP at age 70. Use

Start if the amount is your estimated monthly CPP at the

age you plan to start CPP. MayRetire converts this input into the

correct CPP amount for both age 65 and your selected CPP start

age.

OAS at age 65 (Planning-style input) Enter projected monthly OAS at age 65. MayRetire applies start-age adjustment.

Your current CPP / Your current OAS (Retired and already started) If benefits are already active, enter your current monthly payments instead of age-65 estimates.

Spouse CPP/OAS fields (Couple mode) Use

the same logic for spouse: start ages plus projected amounts (planning)

or current amounts (retired-started). For spouse CPP,

Estimation at: Start means the estimated monthly CPP at the

start of your spouse’s CPP.

CPP Sharing Enabling CPP sharing does not change total household CPP. It changes taxable attribution between spouses and can improve tax efficiency.

Practical guidance:

Additional Income entry. It

will be taxed as regular income to the CPP recipient.

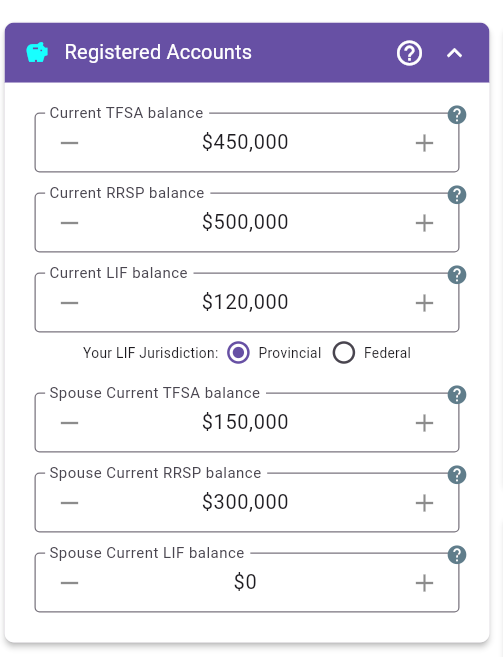

Figure 5: Registered Accounts - Retired Couple

This panel captures registered balances used to fund retirement in a tax-efficient way.

TFSA balance In planning mode, enter expected balance at retirement start. In retired mode, enter current balance. TFSA withdrawals are generally tax-free and often used for late-stage tax control.

RRSP balance In planning mode, enter projected RRSP at retirement start. In retired mode, enter current RRSP/RRIF balance. RRSP/RRIF withdrawals are taxable and central to drawdown-tax planning.

LIF / LIRA balance MayRetire shows LIF or LIRA based on age/status. LIRA is modeled as locked-in pension assets. Upon retirement or age 55 (whichever is later), MayRetire models conversion to LIF and applies legislated withdrawal limits.

LIF Jurisdiction (Provincial / Federal) Set governing regime for LIF calculations. This affects annual minimum/maximum withdrawal limits.

Gradual LIF Unlocking When available for the selected LIF jurisdiction, this option models an annual direct transfer of unused LIF maximum withdrawal room into an RRSP/RRIF. The transferred amount is treated as tax-deferred movement from locked-in funds to unlocked registered funds, not as spendable current-year cash and not as taxable LIF withdrawal income in the projection. In couple mode, the option applies to both partners where each person’s LIF jurisdiction supports the strategy.

Spouse TFSA / RRSP / LIF (or LIRA) (Couple mode) Enter spouse balances separately so MayRetire can optimize household withdrawals and taxation.

Practical guidance:

Note:

help_info.dart; wording above follows the app’s

LIF/LIRA modeling behavior.

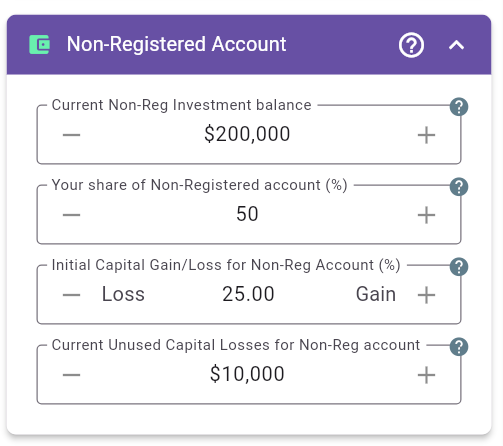

Figure 6: Non-Registered Account

This panel models taxable investment assets and their embedded tax profile.

Current Non-Reg Investment balance Enter total non-registered balance (or projected retirement-start balance in planning mode).

Your share of Non-Registered account (%)

(Couple mode) Defines tax attribution split between spouses.

Example: 50 means income and gains are attributed

50/50.

Initial Capital Gain/Loss for Non-Reg Account (%) Enter unrealized gain/loss as a percentage of average cost base. Example: $50,000 unrealized gain on a $200,000 cost base = 25%. Example: $10,000 unrealized loss on a $100,000 cost base = -10%. This drives capital-gain tax on withdrawals/deemed dispositions.

Current Unused Capital Losses for Non-Reg account Enter carry-forward capital losses that can offset future realized capital gains, reducing projected tax.

Practical guidance:

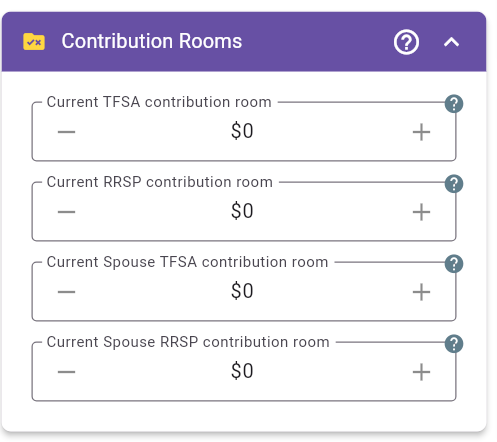

Figure 7: Contribution Rooms

This panel defines how much additional tax-sheltered contribution capacity is available.

Current TFSA contribution room Enter current available TFSA room. MayRetire increases TFSA room annually using the government limit assumption.

Current RRSP contribution room Enter RRSP room from your latest CRA Notice of Assessment. RRSP contributions are modeled as age-limited (through age 71).

Current Spouse TFSA contribution room (Couple mode) Same logic for spouse TFSA room.

Current Spouse RRSP contribution room (Couple mode) Same logic for spouse RRSP room, including age-71 contribution limit.

Practical guidance:

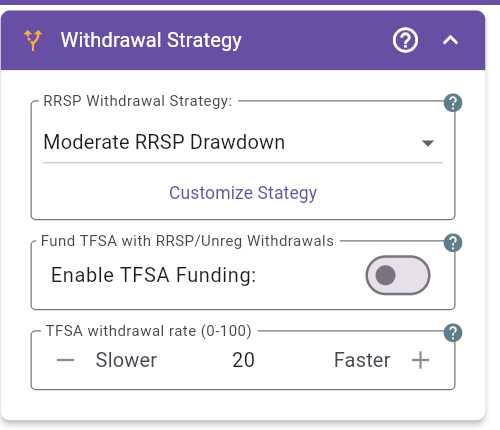

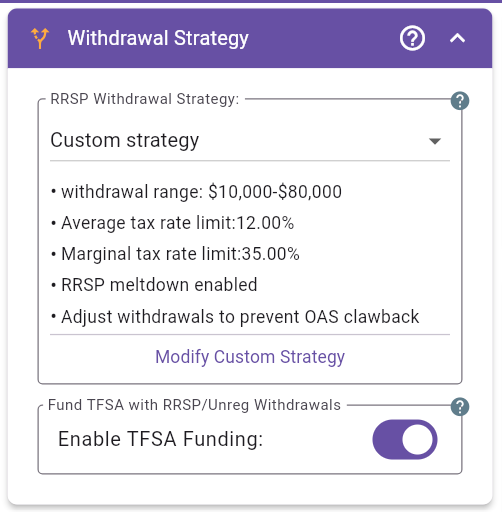

Figure 8: Withdrawal Strategy - Preset

Figure 9: Withdrawal Strategy - Custom Summary

This panel controls account drawdown behavior and tax constraints across RRSP/RRIF, non-registered assets, and TFSA.

RRSP Withdrawal Strategy Choose a predefined

style (Conservative, Moderate,

Progressive, Accelerated) or define a

Custom strategy.

Preset mode Applies a ready profile to speed up scenario testing.

Custom mode Displays your active custom constraints (for example: amount limits, tax limits, meltdown, OAS-clawback adjustment).

Customize Strategy / Modify Custom Strategy Opens the full strategy editor.

Fund TFSA with RRSP/Unreg Withdrawals When enabled, MayRetire may withdraw beyond immediate spending needs to use TFSA room. TFSA can become a destination account for tax-efficient repositioning.

TFSA withdrawal rate (0 to 100) (shown when TFSA funding is disabled) Controls the share of remaining shortfall covered from TFSA. Example: if remaining shortfall is $10,000 and rate is 20, TFSA contributes about $2,000 before fallback rules apply.

Practical guidance:

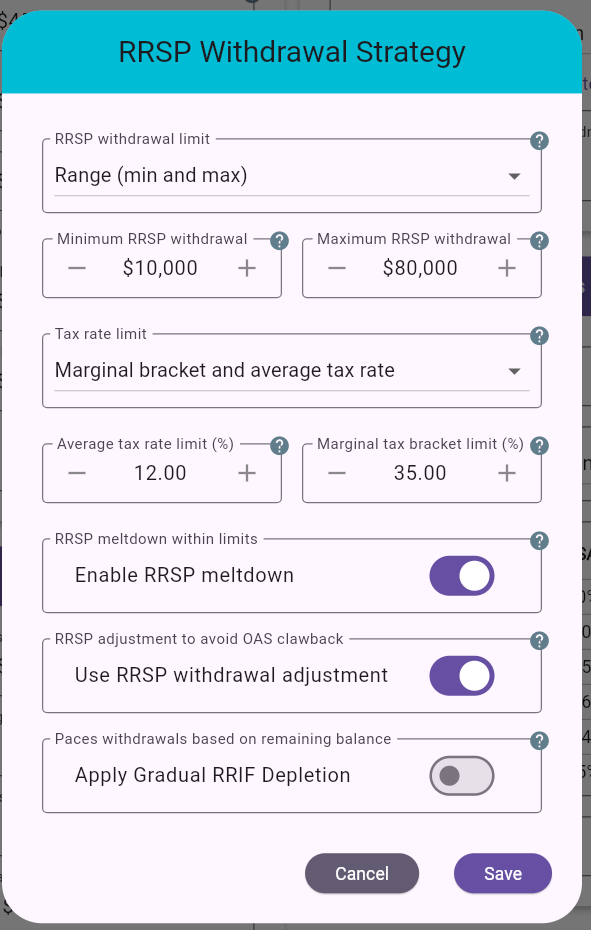

Figure 10: RRSP Withdrawal Strategy Dialog

Use this dialog to define annual withdrawal limits and tax targeting behavior.

RRSP withdrawal limit Options include range, min-only, max-only, fixed amount, or no amount limit.

Minimum RRSP withdrawal / Maximum RRSP withdrawal Used when floor/ceiling control is enabled.

Tax rate limit Choose tax control mode:

Average tax rate limit (%) Best-effort ceiling for average effective tax burden.

Marginal tax bracket limit (%) Best-effort ceiling for marginal tax on the next withdrawal dollar.

Enable RRSP meltdown Allows RRSP withdrawals above required income (within limits), often to reduce future tax concentration. Excess can be redirected to TFSA (if room exists) or non-registered account.

Use RRSP withdrawal adjustment (avoid OAS clawback) Reduces RRSP withdrawals where possible to lower OAS clawback while respecting mandatory minima.

Apply Gradual RRIF Depletion Adds a minimum pace intended to avoid very large end-of-plan RRIF balances and associated estate-tax spikes.

Conditional options you may also encounter Bridging before CPP/OAS, fixed-amount override behavior, RRSP tax-cost limit, and other mode-specific controls.

Figure 11: Investment Assumptions - Simplified Method

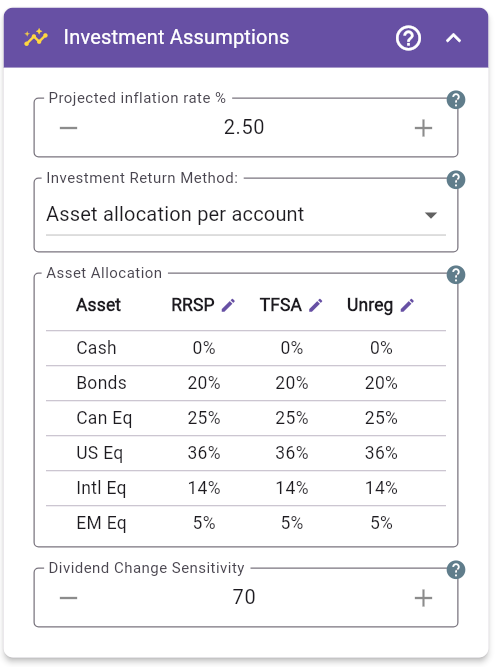

Figure 12: Investment Assumptions - Asset Allocation per Account

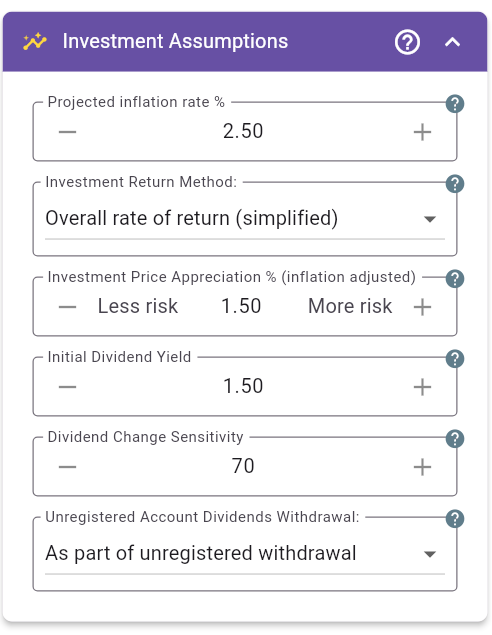

This panel sets inflation and return modeling assumptions that feed income, tax, and confidence-level projections.

Projected inflation rate (%) Long-term inflation assumption. MayRetire uses inflation to keep results in real-dollar terms and for calculations that require nominal tracking (for example, capital-gain tax effects).

Investment Return Method Choose one of two approaches:

Overall rate of return (simplified): enter one real

appreciation rate plus one dividend yield for the portfolio.Asset allocation per account: define account-level

asset mixes; MayRetire derives returns using FP Canada Projection

Assumption Guidelines.Note:

Overall rate of return (simplified)is a legacy what-if method. It uses synthetic, portfolio-wide assumptions and can be less realistic than account-level asset allocation, especially at high return inputs.

This mode is best for quick scenario testing (“what if returns are X?”) rather than selecting a recommended long-term portfolio.

Investment Price Appreciation % (inflation adjusted) Expected real capital growth excluding dividends. A value near 0 means growth roughly keeps pace with inflation.

Initial Dividend Yield Expected annual dividend income as a percent of portfolio value.

Dividend Change Sensitivity (DCS) Controls how dividend amounts respond to price changes. Example: DCS 50 means a 10% price move changes dividends by about 5% in the same direction. Example: if price rises 20%, DCS 50 implies ~10% higher dividends. Example: if price falls 30%, DCS 50 implies ~15% lower dividends. At DCS 100, dividend yield as a percentage of price remains roughly constant.

Unregistered Account Dividends Withdrawal Choose one:

Withdraw dividends first: prioritize dividend cash flow

before principal sales.As part of unregistered withdrawal: treat dividends and

principal as a pooled source.

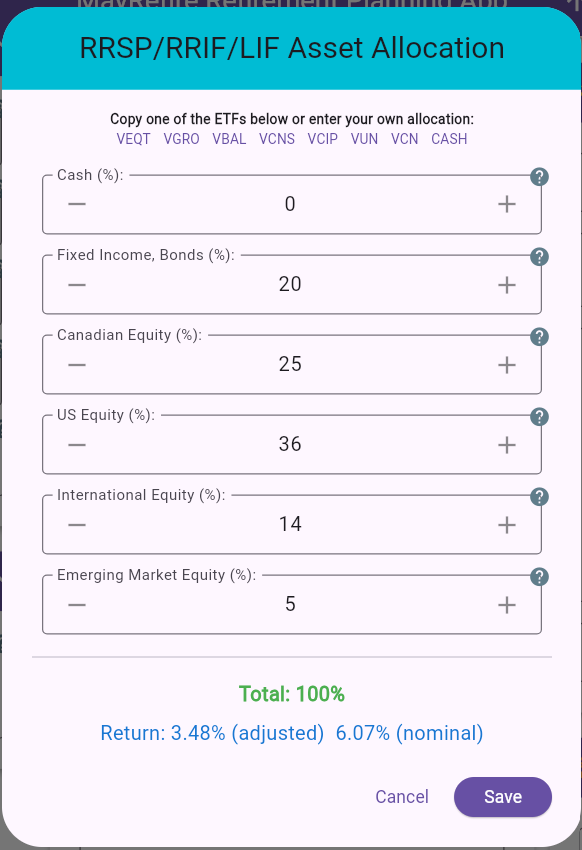

Figure 13: Asset Allocation Dialog (RRSP/RRIF/LIF)

In this method, users input allocation weights, not return rates.

Asset buckets and tax interpretation in non-registered context:

Editor features:

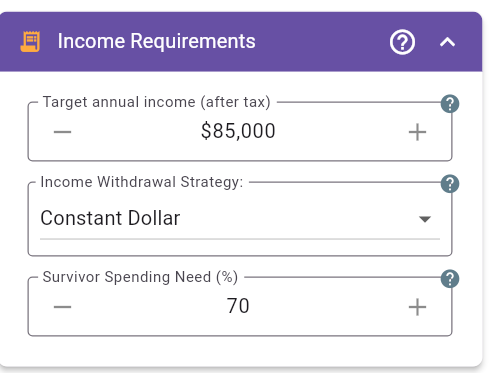

Figure 14: Income Requirements - Constant Dollar

Figure 15: Income Requirements - Flexible

This panel defines baseline after-tax income targets in today’s dollars (real purchasing power). Use it to separate preferred lifestyle spending from the minimum spending level you want the plan to protect.

Target annual income (after tax) Preferred after-tax income level for normal retirement lifestyle spending.

Income Withdrawal Strategy

Constant Dollar: stable real spending target year to

year.Flexible: income can adjust between target and minimum

based on plan strength and return conditions.Minimal annual income (after tax) (shown in Flexible mode) Lower after-tax income floor MayRetire attempts to protect in weak scenarios.

Survivor Spending Need (%) (Couple mode) Percent of combined household budget the surviving spouse is expected to need. Common planning range is roughly 60% to 70%, because many fixed costs remain after one partner passes.

Flexible income is best understood as a planning guardrail, not an automatic real-life withdrawal rule. The target income represents preferred lifestyle spending, while the minimum income represents a lower level the plan should try to preserve when markets, balances, or other assumptions are under pressure.

For Calculate-style runs, MayRetire first tests whether the plan can support the full target income. If the target is not sustainable, it tests whether the minimum income is sustainable. If the minimum works, MayRetire searches between the minimum and target to find the highest income level that can still keep the plan funded under the selected assumptions or return sequence.

For simulation and backtesting runs, MayRetire also compares each scenario’s current asset path against a reference baseline. If assets are tracking below the reference path, the current year’s flexible income is reduced toward the minimum. If assets are healthy, income can remain closer to the target. The intent is to spend more when the plan has room and less when markets or balances are under pressure.

In practice, do not treat the flexible result as an exact spending rule for every future year. A more practical approach is to create an updated plan at least annually using current account balances, current pension and income details, updated debt or insurance assumptions, current tax context, and any changed priorities. At that point, you may also decide whether the target and minimum income range itself should move up or down.

The first year of the updated projection can then be used as guidance for the upcoming year’s cash flow, including planned spending, account withdrawals, taxes, contributions, debt payments or advances, and other income sources. In this sense, MayRetire helps answer: given where the plan stands now, what cash-flow plan looks reasonable for the next year while preserving the long-term plan?

Practical guidance:

Additional Withdrawals, such as travel years, vehicle

replacement, renovations, or health-care support.

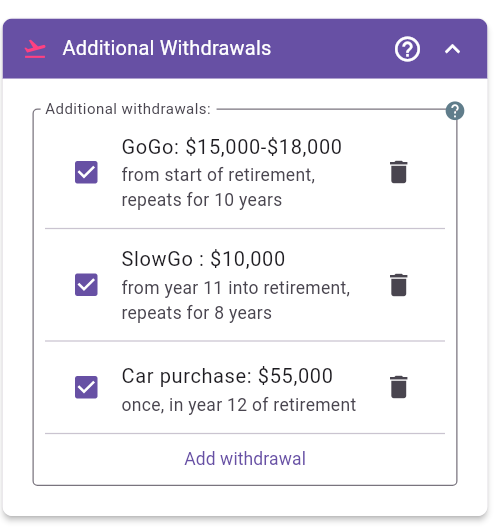

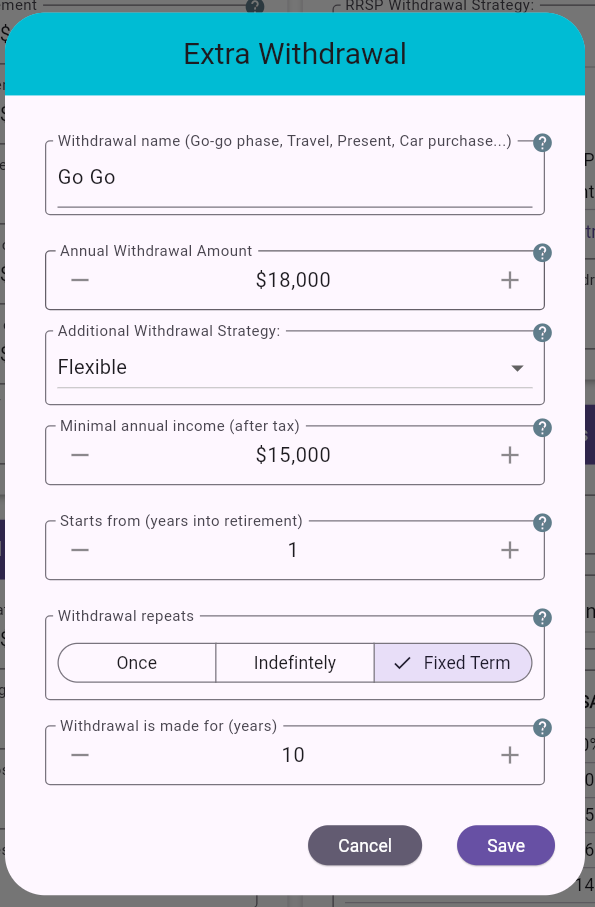

Figure 16: Additional Withdrawals panel with multiple planned withdrawals

This section lets you model discretionary or phase-specific spending that sits on top of your base income target. Typical use cases include travel phases, gifts, major purchases, family support, or one-time events.

Panel behavior:

Add withdrawal creates a new item using the edit

dialog.

Figure 17: Additional Withdrawal edit dialog

Withdrawal name Use a descriptive label (for

example: Go-Go, Slow-Go,

Car purchase, Family support).

Annual Withdrawal Amount Target yearly amount for this withdrawal item.

Additional Withdrawal Strategy Choose one:

Constant Dollar: keeps the withdrawal amount fixed in

real terms.Flexible: allows the withdrawal to vary when needed,

subject to a minimum floor.Minimal annual income (after tax) (shown when strategy is Flexible) Minimum after-tax amount you still want to preserve for this withdrawal category.

Starts from (years into retirement) Offset from retirement start.

1 means first retirement year.11 means withdrawal starts in year 11 of

retirement.Withdrawal repeats Choose recurrence mode:

Once: one-time withdrawal.Indefinitely: continues through the full remaining

plan.Fixed Term: continues for a specified number of

years.Withdrawal Frequency (shown when the withdrawal is not Once) Choose how often the withdrawal occurs within the selected period:

Every year: applies annually.Every 2 years, Every 3 years, etc.:

applies only in matching interval years, starting from the selected

start year.Withdrawal is made for (years) (shown for Fixed Term) Number of years the withdrawal repeats.

Practical guidance:

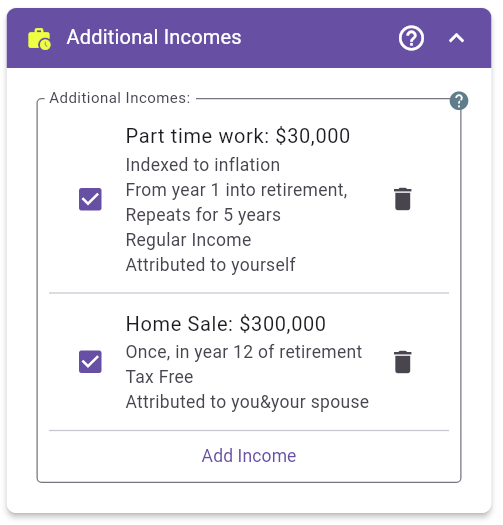

Figure 18: Additional Incomes panel with recurring and one-time income items

This section models non-portfolio income sources you expect during retirement. Common examples include part-time work, annuities, a business sale, inheritances, and other cash inflows.

Panel behavior:

Add Income opens the edit dialog.

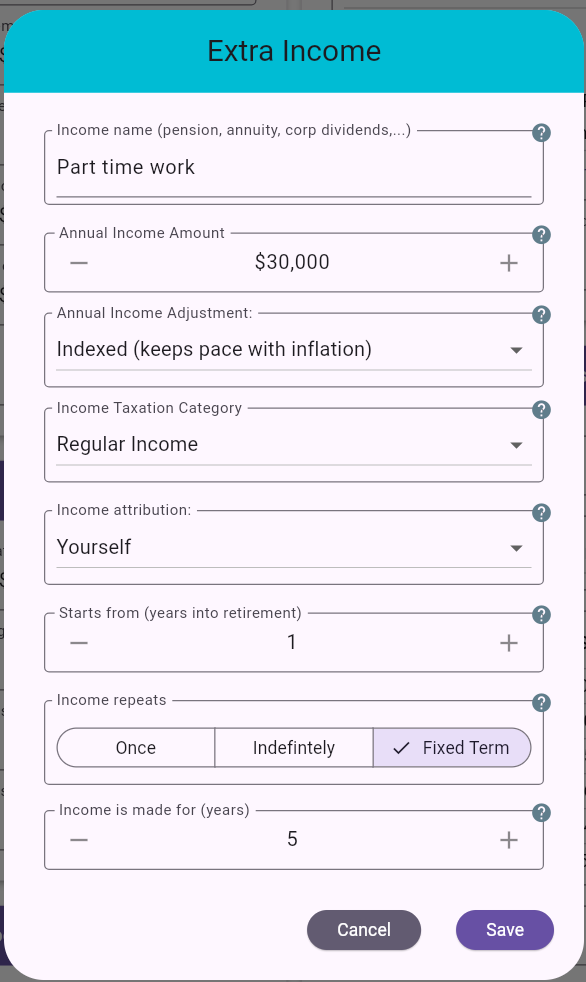

Figure 19: Additional Income edit dialog

Income name Use a clear label (for example:

Part-time work, Annuity,

Home sale, Inheritance).

Annual Income Amount Annual amount for this income stream. For one-time events, this is the one-time value.

Annual Income Adjustment Choose how the amount evolves over time:

Indexed (keeps pace with inflation): preserves

purchasing power in real terms.Fixed nominal (if selected): amount stays flat in

dollars and loses real value over time.Income Taxation Category Controls how the income

is taxed in projections (for example regular income vs tax-favoured

categories). Choose the category that best matches the real tax

treatment of this source. Under Taxed, you can choose:

Full amount: the entire income is taxed using the

selected category.Partially (annuity, etc.): only the entered taxable

percentage is taxed using the selected category, and the remainder is

treated as tax-free. This option was added mainly for annuities and

similar income streams where only part of each payment is taxable.Income attribution Assign income to

Yourself, Spouse, or both, depending on who

receives it. This matters for personal tax calculations and cash-flow

allocation in couple plans.

Starts from (years into retirement) Timing offset from retirement start.

1 means first retirement year.12 means year 12 of retirement.Income repeats Choose recurrence pattern:

Once: one-time income event.Indefinitely: repeats every year through the remaining

plan.Fixed Term: repeats for a selected number of

years.Income is made for (years) (shown for Fixed Term) Number of years that the income repeats.

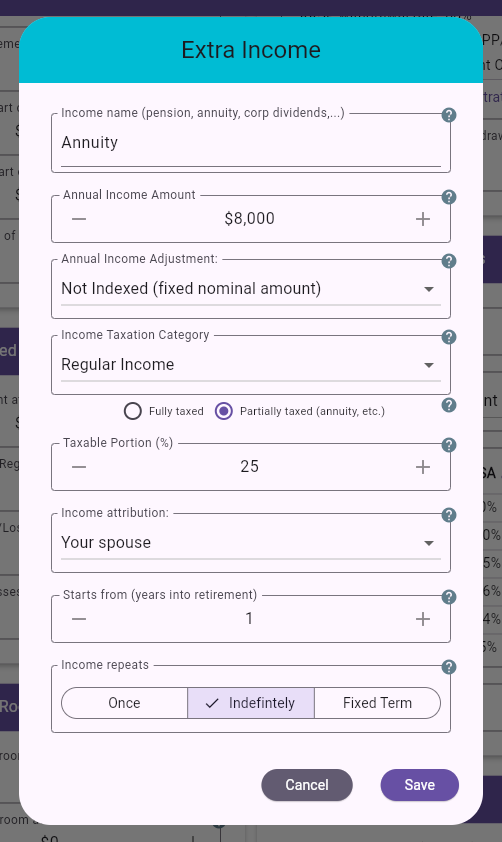

Annuity example:

Taxed: Partially (annuity, etc.).

Figure 20: Additional Income dialog showing a partially taxed annuity example

Practical guidance:

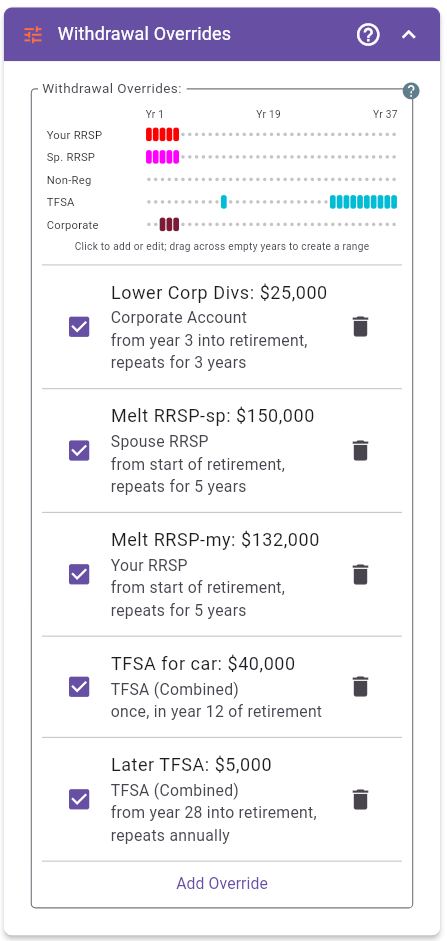

Figure 21: Withdrawal Overrides panel with account timeline and configured override periods

Withdrawal Overrides let you tailor selected account withdrawals when your preferences or planning objectives are not readily expressed through the automatic strategy settings. For example, you may prefer predictable, round-number RRSP withdrawals during the first years of retirement; reduce corporate dividends in a rental-property sale year to avoid layering dividend income on top of the sale’s taxable income; or fund a large purchase, such as a car, from the TFSA without disrupting an otherwise smooth taxable-income and tax-rate profile. Overrides can therefore support personal preferences, manual coordination of unusual financial events, and simple mental accounting for specific goals.

Withdrawal Overrides are different from Additional Withdrawals:

Override amounts are entered in today’s dollars.

The timeline provides a compact view of overrides across the retirement plan:

Yr 1 is the first year of retirement, not

a calendar year.The timeline colours distinguish account types; they do not indicate whether the requested withdrawal was fully achieved. Review the detailed annual projections and income results to see the actual outcome.

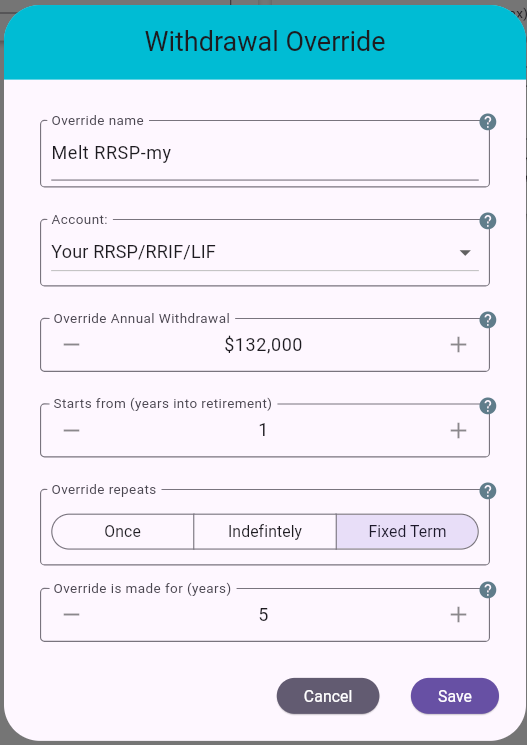

Figure 22: Withdrawal Override dialog with account, amount, start, and duration settings

Override name Enter a short, descriptive

reminder of why the override exists, such as

Early RRSP bridge, Preserve TFSA, or

Corporate dividends.

Account Select the account whose automatic withdrawal should be overridden:

Override Annual Withdrawal Requested annual withdrawal from the selected account. Zero is allowed and can be used to prevent discretionary withdrawals during the override period, subject to mandatory RRIF/LIF rules.

Starts from (years into retirement)

Retirement-year offset when the override begins. 1 applies

in the first year of retirement.

Override repeats Choose the duration:

Once: applies for one retirement year.Indefinitely: applies through the remainder of the

plan.Fixed Term: applies for the specified number of

years.Override is made for (years) (shown for Fixed Term) Number of consecutive retirement years for which the override applies.

An override is a requested account-withdrawal setting, not a guarantee that the exact amount will appear in the results. MayRetire still coordinates all income sources against the annual after-tax income target and applicable account rules.

The requested amount may not be fully used when:

Conversely, restricting withdrawals can leave annual income below the target even when money remains in an overridden account. This is intentional: once an override limits an account, MayRetire does not automatically exceed that limit merely to eliminate the income deficit.

Account-specific considerations:

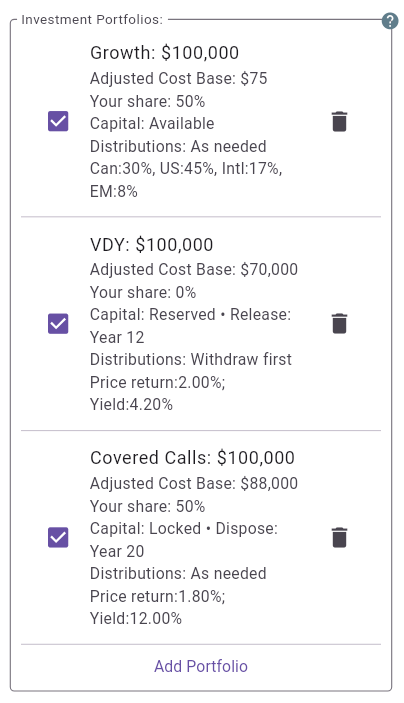

Figure 23: Investment Portfolios panel with multiple taxable portfolios

Investment Portfolios are optional taxable portfolios that coexist with the regular non-registered account. They are useful when you want a separate asset mix, tax attribution, access rule, or distribution policy for part of the household’s taxable assets.

Note: Investment Portfolios are supported when

Asset allocation is enabled.

Common uses:

Panel behavior:

Add Portfolio opens the multi-tab edit dialog.

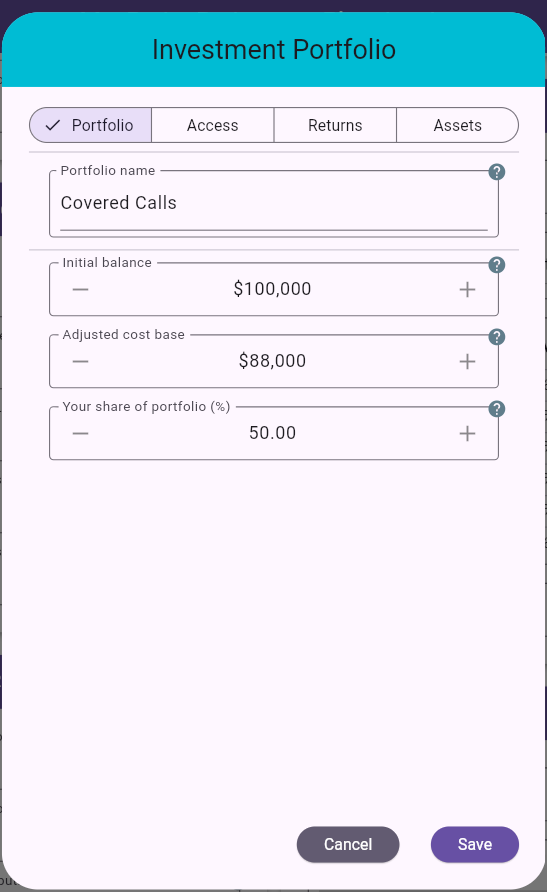

Figure 24: Investment Portfolio dialog - Portfolio tab

Portfolio name Use a clear label (for example:

Growth, Income ETF,

Emergency fund, or

Spouse taxable portfolio).

Initial balance Current market value of this portfolio, or the projected retirement-start value in planning mode.

Adjusted Cost Base Tax cost base of the portfolio. MayRetire uses this to estimate capital gains or losses when capital is withdrawn, the portfolio is liquidated, or the estate is calculated. In real-dollar projections, ACB is adjusted for inflation over time because the nominal tax cost base does not automatically grow with inflation.

Your share of portfolio (%) (Couple mode) Ownership/tax attribution assigned to you. The remainder is attributed to spouse while both spouses are alive.

Practical guidance:

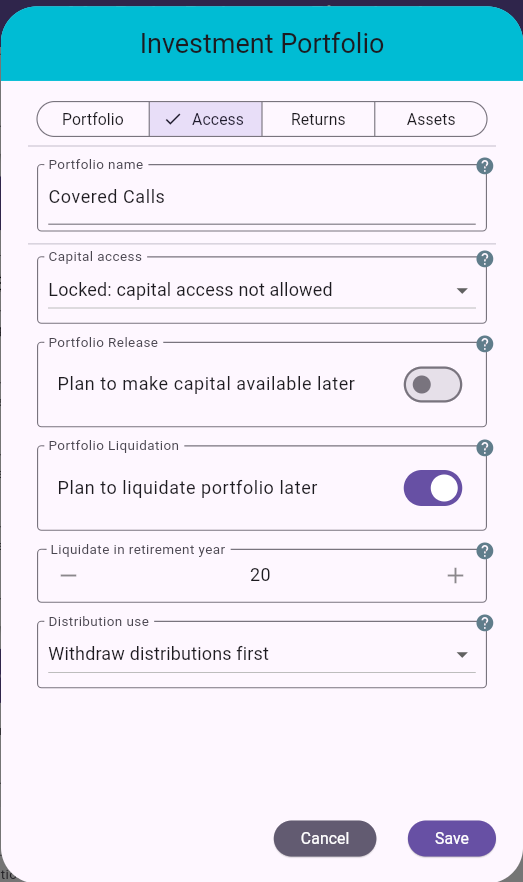

Figure 25: Investment Portfolio dialog - Access tab

This tab controls whether capital and distributions can be used to fund retirement income.

Capital access

Available: capital can be used like regular

non-registered assets.Reserved: capital is used only after regular

non-registered capital and available portfolio capital are

exhausted.Locked: capital is not used for retirement spending

unless the portfolio is later released or liquidated.Portfolio Release When enabled, a reserved or locked portfolio can become available in a selected retirement year. Release changes the access rule but keeps the portfolio intact.

Portfolio Liquidation When enabled, MayRetire sells the portfolio in the selected retirement year, realizes the capital gain/loss, and moves the proceeds into the regular non-registered account.

Distributions

Withdraw first: taxable distributions are consumed

before other income-gap withdrawals.As needed: distributions remain available and are used

only when needed to meet the income target.Reinvest only (shown for Locked capital):

distributions are still taxable, but they are not available for

retirement spending and remain invested in the portfolio.Practical guidance:

Reserved for assets intended as a last-resort

buffer.Locked for assets you do not want the

retirement-income engine to spend.Reinvest only when a locked portfolio should stay

outside retirement cash flow, including its annual distributions.

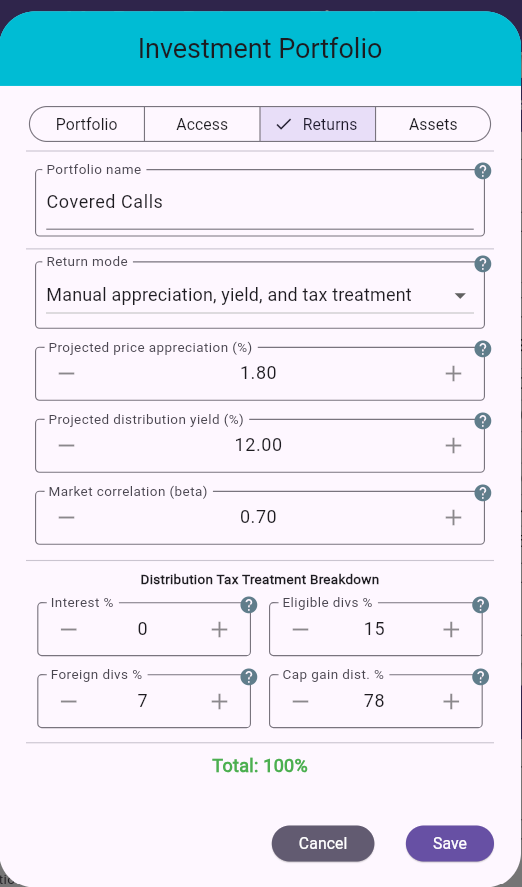

Figure 26: Investment Portfolio dialog - Returns tab

This tab defines how the portfolio produces price growth and taxable distributions.

Return mode

Asset allocation using FP Canada Assumptions: return

and distribution assumptions come from the portfolio’s asset mix.Manual appreciation, yield and tax treatment: you enter

projected price appreciation, distribution yield, and tax-treatment

breakdown.Projected Price Appreciation (%) (Manual mode) Expected real price growth before distributions.

Projected Distribution Yield (%) (Manual mode) Expected annual distribution as a percentage of portfolio value.

Market correlation (Beta) (Manual mode) Controls how strongly the manual portfolio responds to market behavior from the reference allocation in simulations. A higher value makes the portfolio move more with the reference allocation; lower or negative values reduce or invert that relationship.

Distribution Tax Treatment Breakdown (Manual mode) Split distributions across taxable categories such as interest, eligible dividends, foreign dividends, and capital gain distributions. The components must total 100% before the dialog can be saved.

Practical guidance:

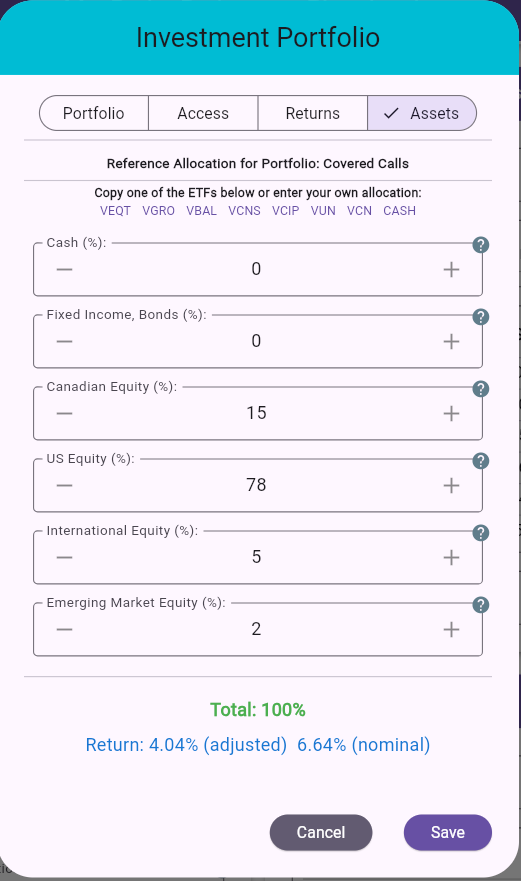

Figure 27: Investment Portfolio dialog - Assets tab

This tab sets the portfolio’s asset allocation.

In asset-allocation return mode, this allocation directly drives expected price return and distribution assumptions. In manual return mode, it acts as the reference allocation used for market correlation and simulation behavior.

Asset allocation inputs Set portfolio mix across

Cash, Fixed Income/Bonds,

Canadian Equity, US Equity,

International Equity, and

Emerging Market Equity.

ETF shortcuts Quick presets for common ETF-style allocations.

Total % check Allocation must total 100%.

Practical guidance:

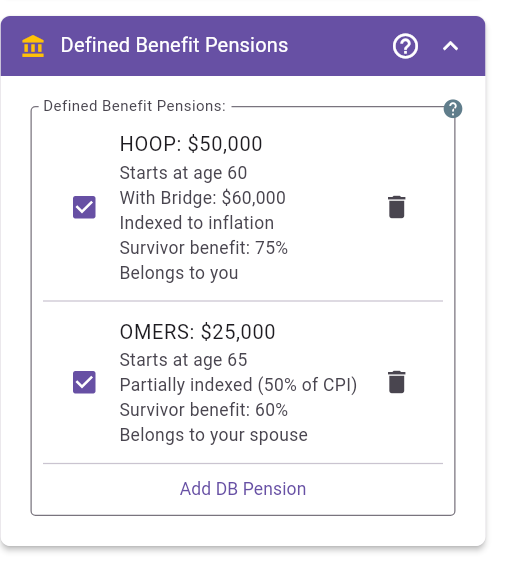

Figure 28: Defined Benefit Pensions panel with multiple pension records

Use this section for employer pensions that provide predictable lifetime income. Properly entering bridge benefits, indexation, and survivor percentage is important because these settings directly affect long-term cash flow and estate outcomes.

Panel behavior:

Add DB Pension opens the pension edit dialog.

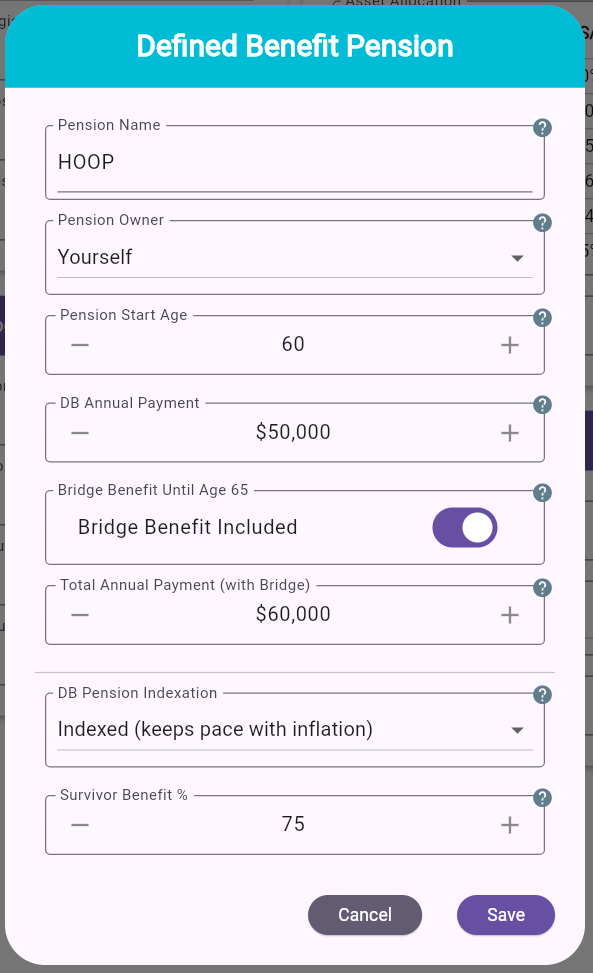

Figure 29: Defined Benefit Pension edit dialog

Pension Name Use a clear plan name (for example:

HOOPP, OMERS, Teachers,

Employer DB Plan).

Pension Owner Select who receives this pension

(Yourself or Spouse). Owner selection affects

tax calculation and survivor planning in couple scenarios.

Pension Start Age Age when payments begin.

DB Annual Payment Base annual lifetime payment (excluding temporary bridge benefit).

Bridge Benefit Until Age 65 Enable this if the plan pays a temporary top-up before age 65.

Total Annual Payment (with Bridge) (shown when bridge is enabled) Combined annual payment before age 65, including base pension plus bridge amount.

DB Pension Indexation Defines how pension payments change over time. Common options include:

Indexed (keeps pace with inflation): payment rises with

CPI to preserve purchasing power.Not indexed: payment is flat in nominal dollars.Partially indexed: payment tracks only part of

CPI.Custom fixed rate: payment rises by a fixed nominal

percentage each year.Partial indexing (%) (shown when Partially

indexed is selected) Percent of CPI passed through to pension

increases (for example 50% of CPI).

Fixed annual increase (%) (shown when Custom fixed rate is selected) Nominal annual increase applied each year.

Survivor Benefit % Portion of pension that

continues to the survivor after first death. Typical values are

0, 50, 60, 66,

75, or 100, depending on plan option.

Survivor Bridge Treatment (shown when bridge benefit and survivor benefit are both applicable) Controls how a temporary bridge benefit is treated if the pension owner dies before age 65. Some plans calculate the survivor benefit from the lifetime pension only, while others include the bridge temporarily or permanently. Use your DB pension statement to choose the matching option.

Practical guidance:

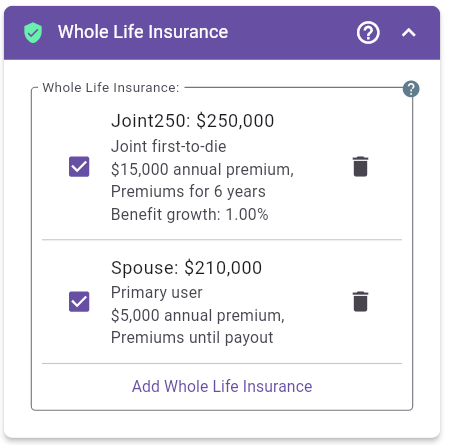

Figure 30: Whole Life Insurance panel with benefit amount summary

Use this section to model whole life insurance policies that have predictable premiums and a predictable death benefit. This includes participating whole life, non-participating whole life, and Term-to-100 style policies. MayRetire does not attempt to model Universal Life mechanics.

Insurance can affect the plan in three ways:

Panel behavior:

Add Insurance opens the insurance edit dialog.

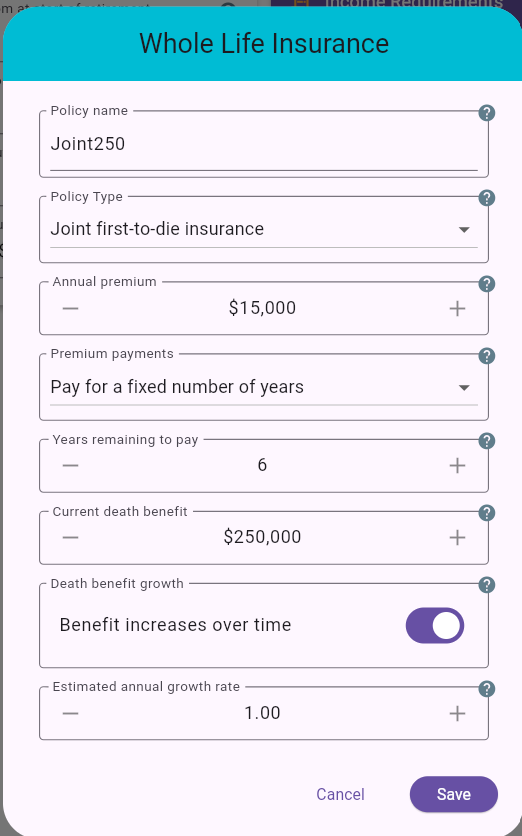

Figure 31: Whole Life Insurance edit dialog

Policy name Use a clear name for the policy,

such as Whole Life, Participating WL, or the

insurer name.

Policy Type (Couple mode) Choose when the policy pays out:

Your life insuranceSpouse's life insuranceJoint first-to-die insuranceJoint last-to-die insuranceIn single plans, MayRetire treats the policy as your own life insurance and does not show the policy-type selector.

Annual premium Fixed nominal premium paid each year while premiums are still required. Because this is a nominal amount, its real cost declines over time with inflation.

Premium payments Choose how long premiums continue:

No more premium payments: the policy is paid up.Payments until insurance payout: premiums continue

while the policy is active in the plan.Pay for a fixed number of years: premiums continue for

a fixed number of remaining years.Years remaining to pay (shown when Premium payments is Pay for a fixed number of years) Number of years premiums still need to be paid.

Current death benefit Current nominal death benefit amount.

Benefit increases over time Turn this on when the death benefit is expected to grow, such as from participating dividends or paid-up additions.

Estimated annual growth rate % (shown when

benefit growth is enabled) Estimated annual nominal growth rate for

the death benefit. Use 0 or leave growth off for a fixed

death benefit.

Practical guidance:

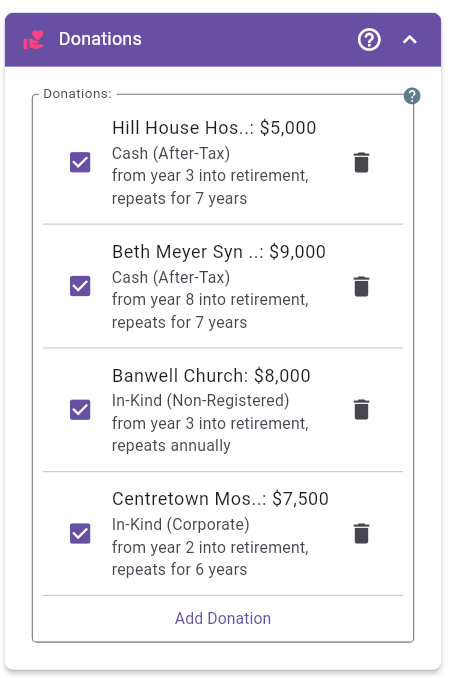

Figure 32: Donations panel with multiple charitable gifts

Use this section to model charitable giving as part of your retirement plan. Donations can be repeated, timed for specific years, and funded in different ways so you can compare both cash-flow impact and tax efficiency.

Panel behavior:

Add Donation opens the donation edit dialog.

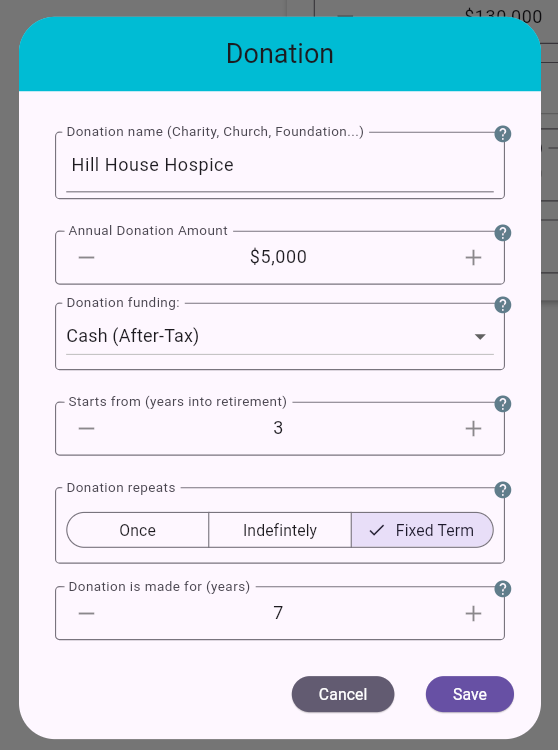

Figure 33: Donation edit dialog

Donation name Use a clear label for the charity

or purpose (for example: Hospital Foundation,

Church, Food Bank,

Family Foundation).

Annual Donation Amount Target amount donated each year while this donation is active.

Donation funding Choose how the gift is funded:

Cash (After-Tax): donation is funded from personal

after-tax cash flow.In-Kind (Non-Registered): donation is made using

eligible securities or funds from the personal non-registered

account.In-Kind (Corporate): donation is made using eligible

securities or funds held inside the corporation.Donation repeats Choose recurrence pattern:

Once: one-time donation event.Indefinitely: repeats every year through the remaining

plan.Fixed Term: repeats for a selected number of

years.Donation is made for (years) (shown for Fixed Term) Number of years the donation repeats.

Practical guidance:

Cash (After-Tax) when you want the donation funded

directly from annual spending cash flow.

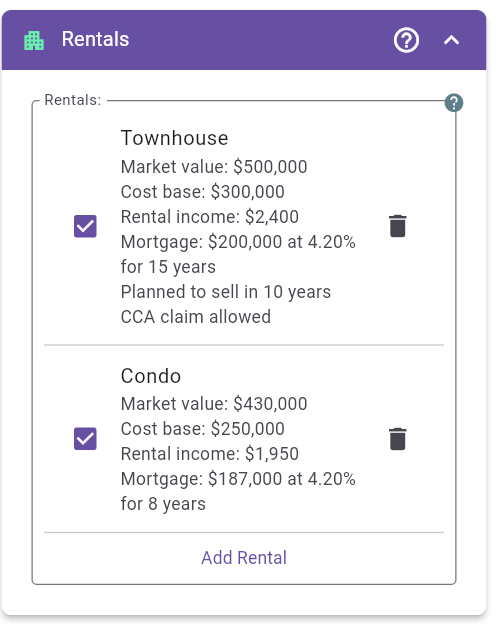

Figure 34: Rentals panel with multiple properties

This section captures rental-property cash flow, financing, planned disposition, and tax treatment so projections include both ongoing rental income and eventual sale/estate outcomes.

Panel behavior:

Add Rental opens the multi-tab rental property

dialog.

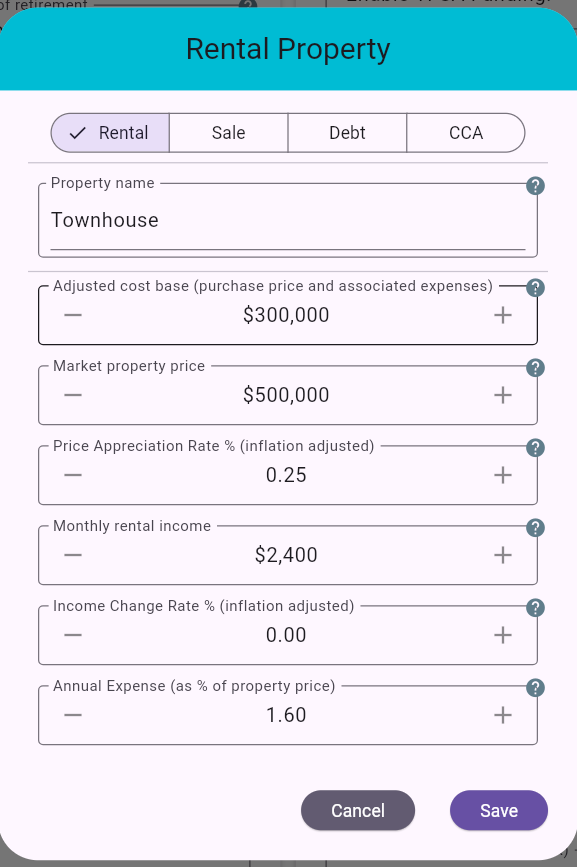

Figure 35: Rental Property dialog - Rental tab

Property name Descriptive label for the property

(for example: Townhouse, Condo,

Duplex).

Adjusted cost base (purchase price and associated expenses) Your tax cost base, including purchase price and eligible acquisition/capital-improvement costs. Used to estimate capital gains when the property is sold.

Market property price Current estimated market value of the property.

Price Appreciation Rate % (inflation adjusted)

Expected long-term real appreciation rate. 0% means the

property grows with inflation only.

Monthly rental income Gross monthly rent before expenses.

Income Change Rate % (inflation adjusted) Real

growth rate of rental income. 0% means rent keeps pace with

inflation. Negative values mean rent lags inflation; positive values

mean it grows faster than inflation.

Annual Expense (as % of property price) Operating costs as a percentage of property value (for example maintenance, condo fees, insurance, vacancy, property tax, and management).

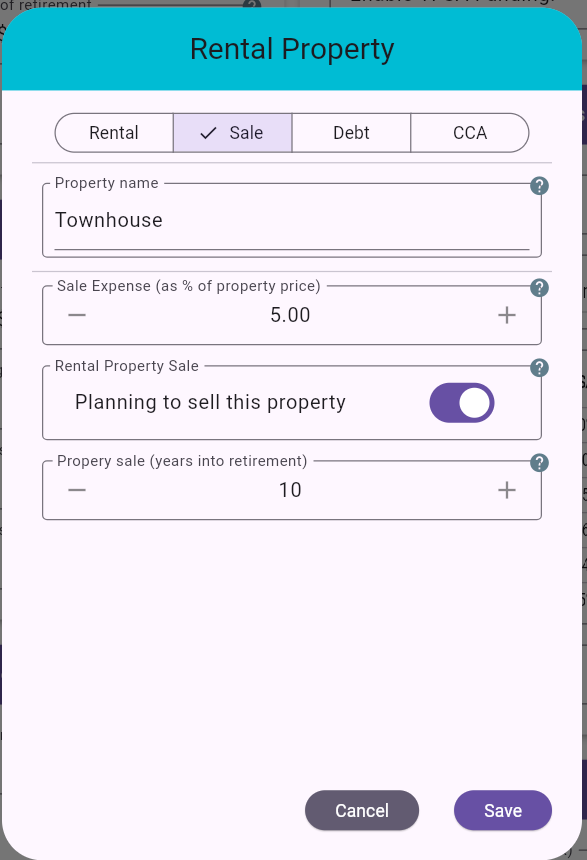

Figure 36: Rental Property dialog - Sale tab

Property name Shown on each tab for context.

Sale Expense (as % of property price) Estimated transaction costs at sale (for example realtor commissions and legal fees).

Rental Property Sale Toggle whether this property is planned to be sold during the planning horizon.

Property sale (years into retirement) (shown

when sale is enabled) Timing of sale relative to retirement start.

10 means planned sale in year 10 of retirement.

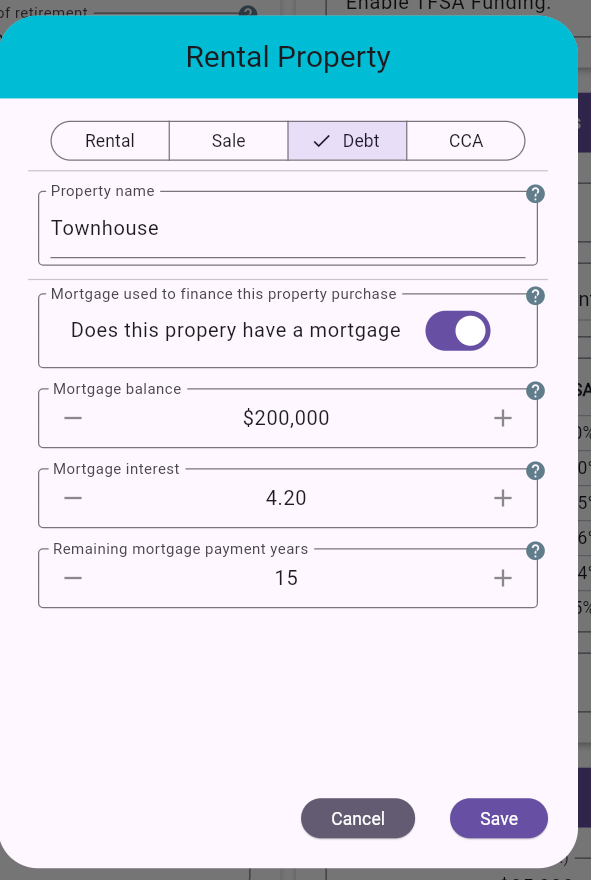

Figure 37: Rental Property dialog - Debt tab

Property name Shown on each tab for context.

Does this property have a mortgage Toggle mortgage financing on/off for this property.

Mortgage balance (shown when mortgage is enabled) Current outstanding mortgage principal.

Mortgage interest (shown when mortgage is enabled) Annual interest rate on the mortgage.

Remaining mortgage payment years (shown when mortgage is enabled) Years left to repay the mortgage.

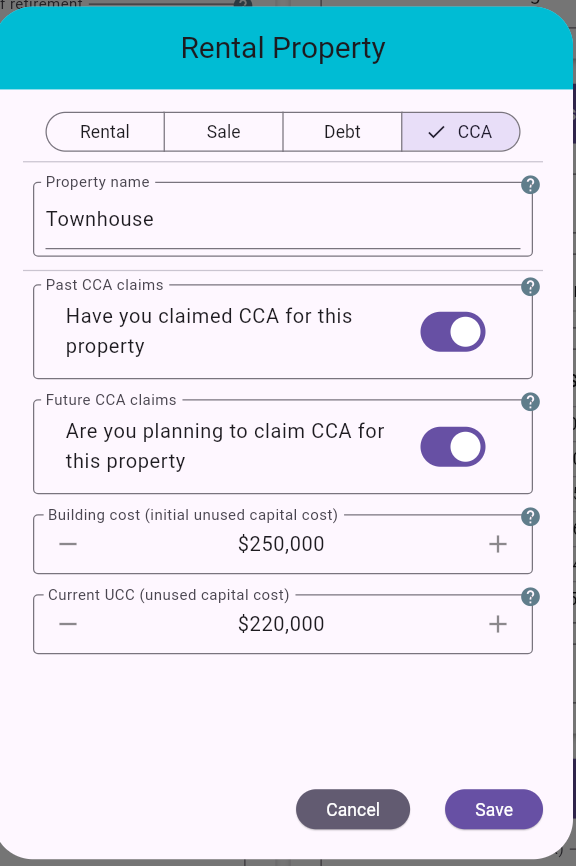

Figure 38: Rental Property dialog - CCA tab

Property name Shown on each tab for context.

Have you claimed CCA for this property Indicates whether CCA was claimed historically.

Are you planning to claim CCA for this property Controls whether future CCA claims are modeled.

Building cost (initial unused capital cost) Original building component used as the starting CCA basis.

Current UCC (unused capital cost) Remaining depreciable balance for future CCA claims.

Practical guidance:

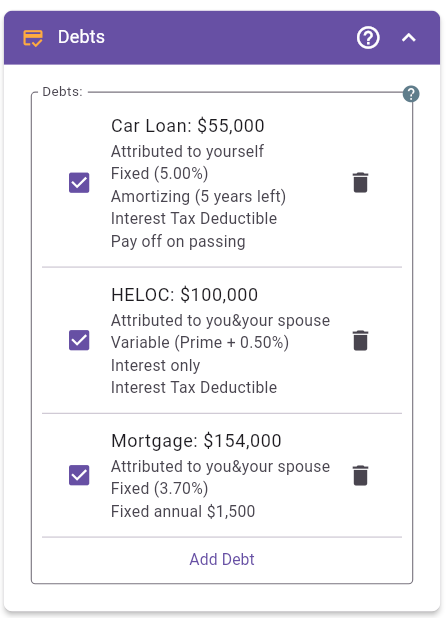

Figure 39: Debts panel with multiple debt items

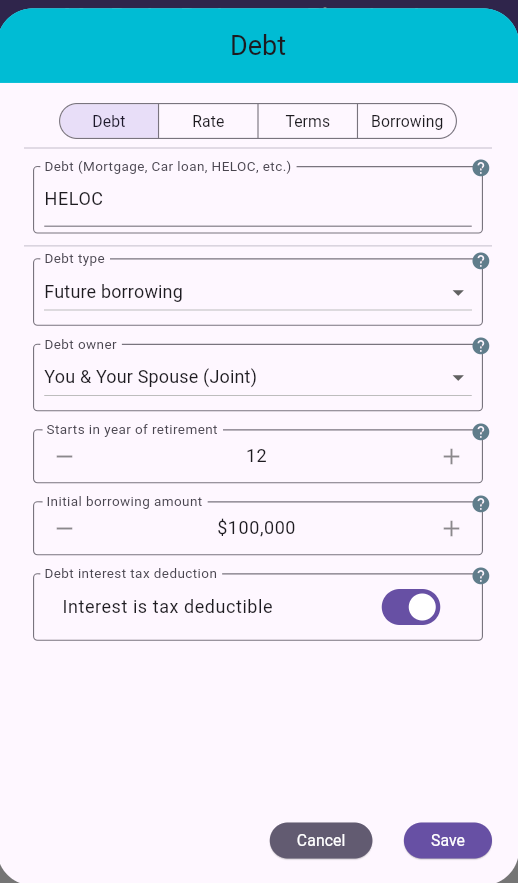

This section lets you model personal or household debt that continues through retirement, such as a mortgage, HELOC, car loan, reverse-mortgage-style borrowing, or other loan. Debt can start as an existing balance at retirement, or it can begin later as future borrowing. Debt affects required cash flow, taxes when interest is deductible, income-source reporting when borrowing proceeds are advanced, and net estate at death.

Panel behavior:

Add Debt opens the debt edit dialog.

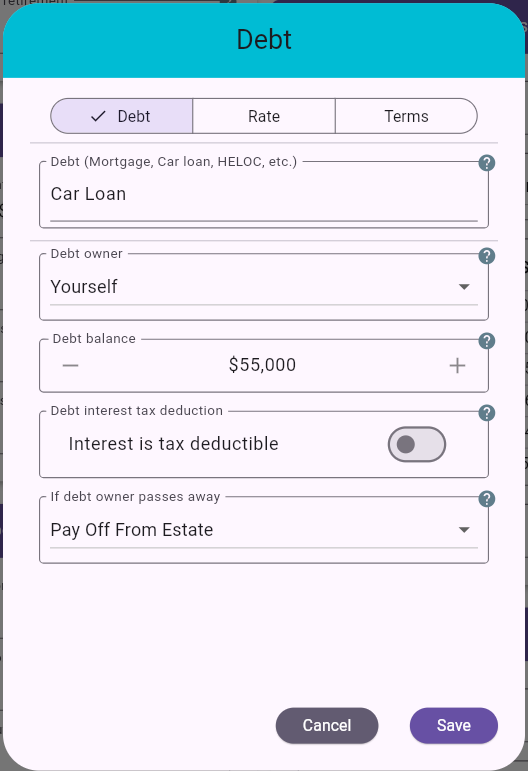

Figure 40: Debt dialog - Debt tab

Debt (Mortgage, Car loan, HELOC, etc.) Use a descriptive name so the debt is easy to identify in the panel and detailed projections.

Debt owner (Couple mode) Choose whether the debt is attributed to you, your spouse, or both jointly. This affects survivor treatment and tax attribution for deductible interest.

Existing debt / Future borrowing Use

Existing debt for a loan that already exists at the start

of the plan. Use Future borrowing for a loan that begins in

a later retirement year.

Debt balance (existing debt) Current outstanding balance at retirement start, or the current balance if already retired.

Starts in year of retirement (future

borrowing) Year when the future debt begins. 1 means

the first year of retirement.

Initial borrowing amount (future borrowing) One-time amount advanced when the future debt begins. This becomes the starting balance of the debt in that year.

Debt interest tax deduction Turn this on only when interest on the debt is legitimately deductible. When enabled, MayRetire applies the deduction according to who the debt is attributed to.

If debt owner passes away (shown only in couple plans for single-owner debt) Choose whether the debt transfers to the surviving spouse or is paid off from estate at first death.

Figure 41: Debt dialog - Future borrowing setup

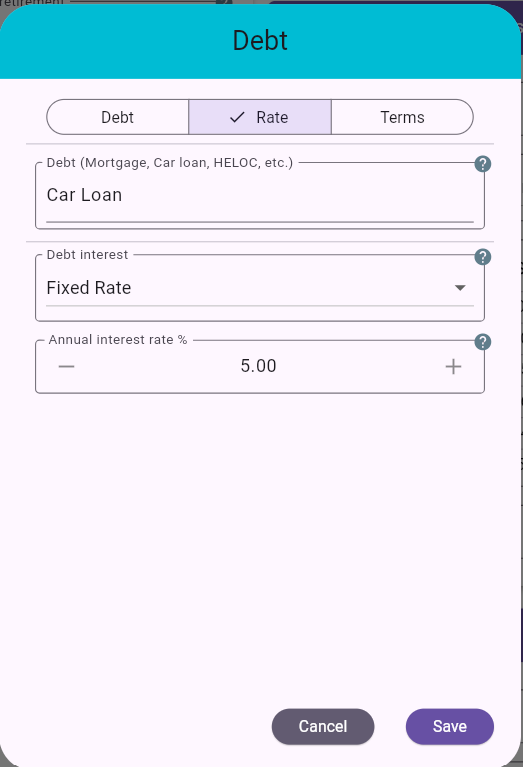

Figure 42: Debt dialog - Rate tab

Debt interest Choose Fixed Rate or

Variable Rate.

Annual interest rate % (shown for fixed rate) Annual fixed borrowing rate used for the debt projection.

Prime spread % (shown for variable

rate) Spread relative to prime. Example: 0.50 means

Prime + 0.50%. Example: -0.75 means

Prime - 0.75%.

Practical note:

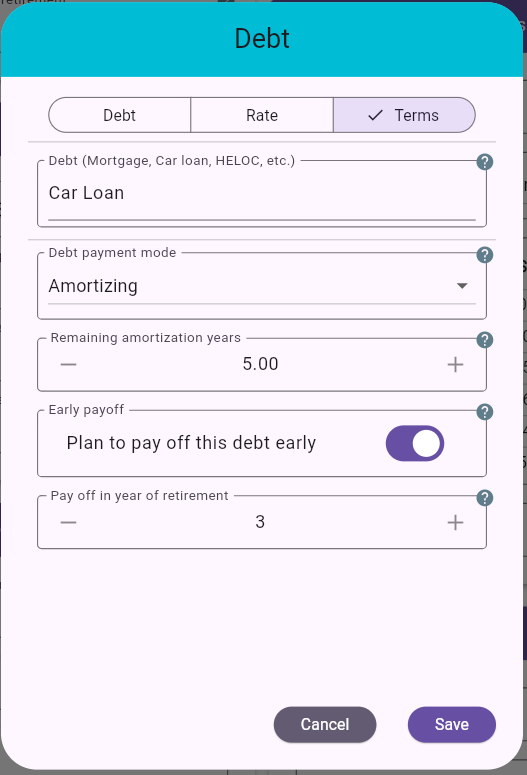

Figure 43: Debt dialog - Terms tab

Debt payment mode Choose one:

AmortizingInterest OnlyFixed Annual PaymentCapitalized InterestRemaining amortization years (shown for amortizing mode) Years left to repay the debt under standard amortizing payments.

Fixed annual payment amount (shown for fixed annual payment mode) Annual amount paid toward the debt each year.

Capitalized interest Interest is added to the debt balance instead of being paid as a regular annual debt payment. Use this for reverse-mortgage-style borrowing or other debt where interest accumulates until payoff, sale, death, or the end of the plan.

Pay off on principal residence sale or downsizing Turn this on when the debt should be fully paid off in the same retirement year that the principal residence is sold or downsized. When this option is enabled, MayRetire hides and ignores the manual early-payoff year because the payoff timing follows the principal residence plan.

Plan to pay off this debt early Use this when you expect to repay the debt in full before its normal schedule ends.

Pay off in year of retirement (shown when

early payoff is enabled) Timing of the extra full payoff relative

to retirement start. 1 means the first year of

retirement.

Practical guidance:

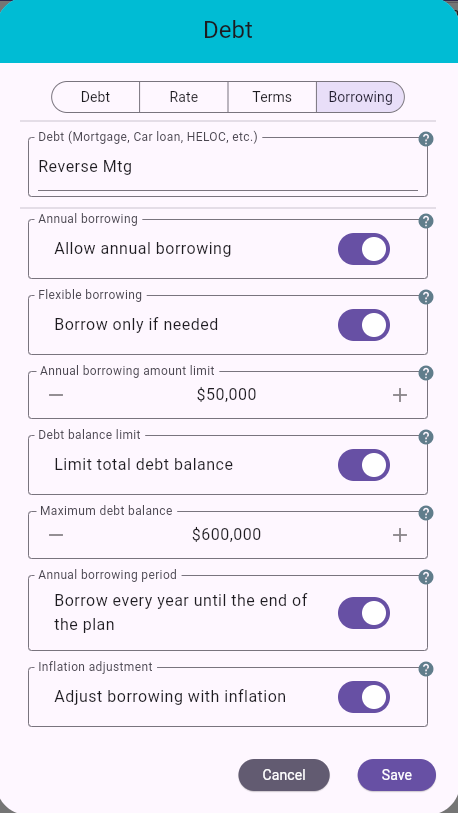

Figure 44: Debt dialog - Borrowing tab

Use this tab when the debt can provide additional scheduled or as-needed borrowing after the initial balance or initial borrowing amount. Borrowing proceeds are treated as debt advances: they increase the debt balance and appear as a separate income source in charts and projections.

Allow annual borrowing Turn this on to add recurring annual borrowing to the debt.

Borrow only when needed Turn this on when the debt is intended as a safety net rather than a planned annual draw. When enabled, MayRetire does not borrow automatically every year. It uses the debt only if other funding sources are not enough to meet the required income level. If the plan never needs the extra cash, no borrowing occurs. This can be useful for testing resilience against less likely but important later-life risks, such as expensive health care, long-term care, or other large support needs. For example, a HELOC, reverse-mortgage-style loan, or borrowing against permanent life insurance may provide a backstop without requiring you to reduce lifestyle assumptions in the base plan. The feature lets you model that safety net while still seeing whether, when, and how much borrowing would actually be needed. This option is available for interest-only and capitalized-interest debts.

Annual borrowing amount / Annual borrowing amount

limit When Borrow only when needed is off, this is

the amount advanced each year while annual borrowing is active. When

Borrow only when needed is on, this is the maximum amount

MayRetire can borrow in a year if other funding is not enough.

Debt balance limit (shown when Borrow only when needed is enabled) Turn this on to cap total borrowing for this debt.

Maximum debt balance (shown when Debt balance limit is enabled) Highest total debt balance allowed for flexible borrowing. If borrowing is adjusted with inflation, this limit is adjusted the same way.

Annual borrowing period Choose whether borrowing continues every year until the end of the plan, or only for a fixed number of years.

Number of borrowing years (shown when borrowing is not until end) Number of years the annual borrowing amount is advanced.

Adjust borrowing with inflation Turn this on when future annual borrowing amounts should increase with inflation.

Practical guidance:

Borrow only when needed

so borrowing happens only if other funding is insufficient.

Figure 45: Principal Residence panel with residence summary

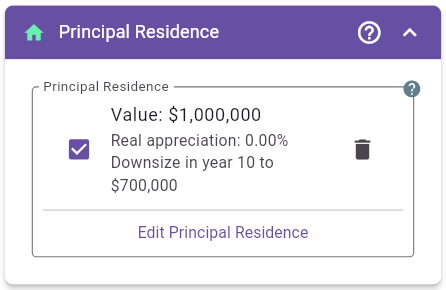

Use this section to model your principal residence separately from investment accounts and rental properties. The residence can be kept to the end of the plan, sold, or downsized to another property. MayRetire treats the principal residence as part of estate value while it is owned, and records sale or downsizing proceeds as cash flow in the disposition year.

Panel behavior:

Edit Principal Residence opens the residence edit

dialog.Remove Principal Residence removes the residence from

the plan.

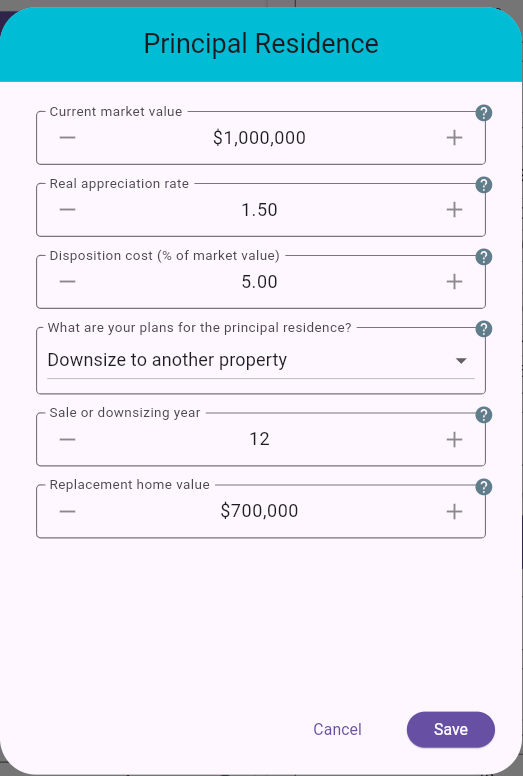

Figure 46: Principal Residence edit dialog

Current market value Estimated current value of the principal residence.

Real appreciation rate Expected annual property appreciation after inflation. This is consistent with rental-property assumptions, where appreciation is entered in real terms.

Disposition cost Estimated selling or disposition cost as a percentage of property value. This reduces estate value and sale/downsize proceeds.

What are your plans for the principal residence? Choose one:

Keep property: residence remains part of the estate

through the plan.Sell property: residence is sold in the configured year

and net proceeds become available cash flow.Downsize to another property: current residence is sold

and replacement home value is deducted from proceeds.Sale / downsizing year Retirement year when the

sale or downsizing occurs. 1 means the first year of

retirement.

Replacement home value (shown when downsizing) Cost of the new principal residence. If replacement value is lower than net sale proceeds, the difference is modeled as residence proceeds. If replacement value is higher, the difference is modeled as a residence shortfall.

Practical guidance:

Keep property when the home is intended to remain

part of the final estate.Sell property when the plan relies on fully

unlocking home equity.Downsize to another property when only part of the

home equity is expected to become available.Pay off on principal residence sale or downsizing.

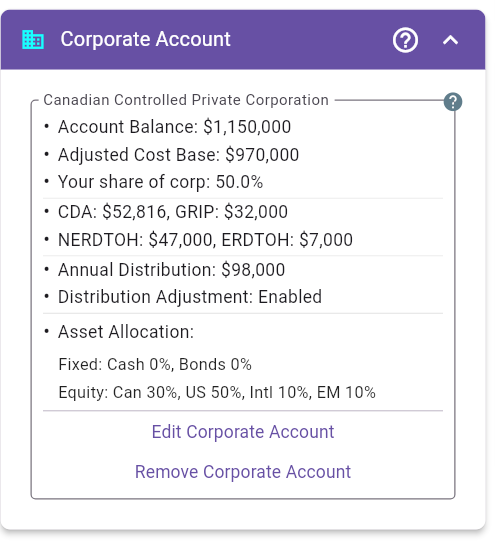

Figure 47: Corporate Account panel with account summary

Use this section for a Canadian Controlled Private Corporation (CCPC) investment account that supports retirement funding through dividends and tax-efficient corporate distributions.

Panel behavior:

Edit Corporate Account opens a 3-tab dialog

(Account, Assets,

Dividends).Remove Corporate Account deletes the corporate-account

setup from the plan.

Figure 48: Corporate Account panel when no corporate account is configured

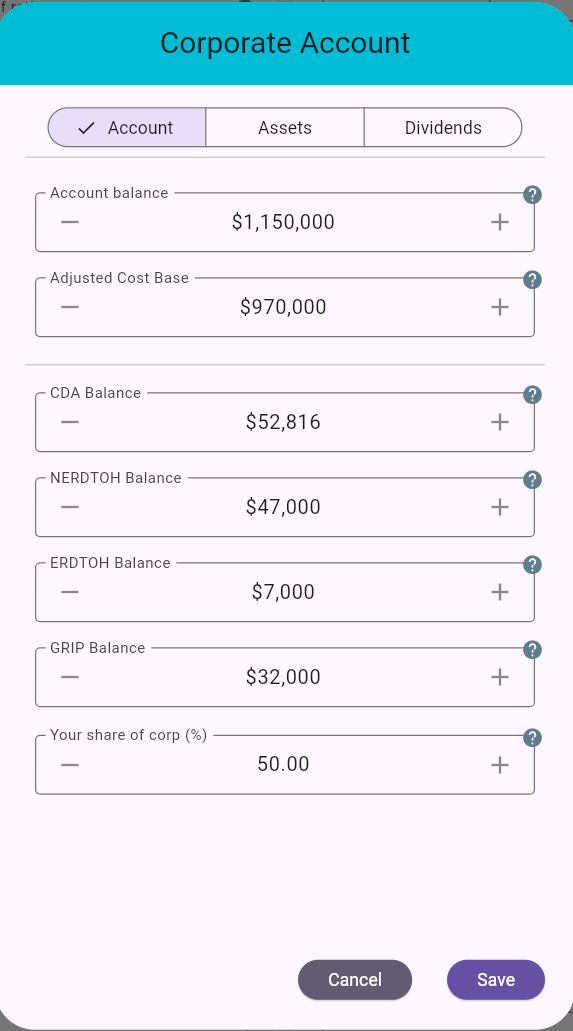

Figure 49: Corporate Account dialog - Account tab

Account balance Current market value of the corporation’s investment portfolio.

Adjusted Cost Base Tax cost base of corporate investments (purchase cost plus acquisition costs), used to calculate capital gains when assets are sold.

CDA Balance Capital Dividend Account balance available for tax-free capital dividends.

NERDTOH Balance Non-Eligible Refundable Dividend Tax on Hand. Represents refundable corporate tax generally recovered when non-eligible dividends are paid.

ERDTOH Balance Eligible Refundable Dividend Tax on Hand. Represents refundable corporate tax generally recovered when eligible dividends are paid.

GRIP Balance General Rate Income Pool balance. Determines how much can be paid as eligible dividends.

Your share of corp (%) Your ownership percentage. In couple mode, the remainder is treated as spouse ownership for attribution purposes.

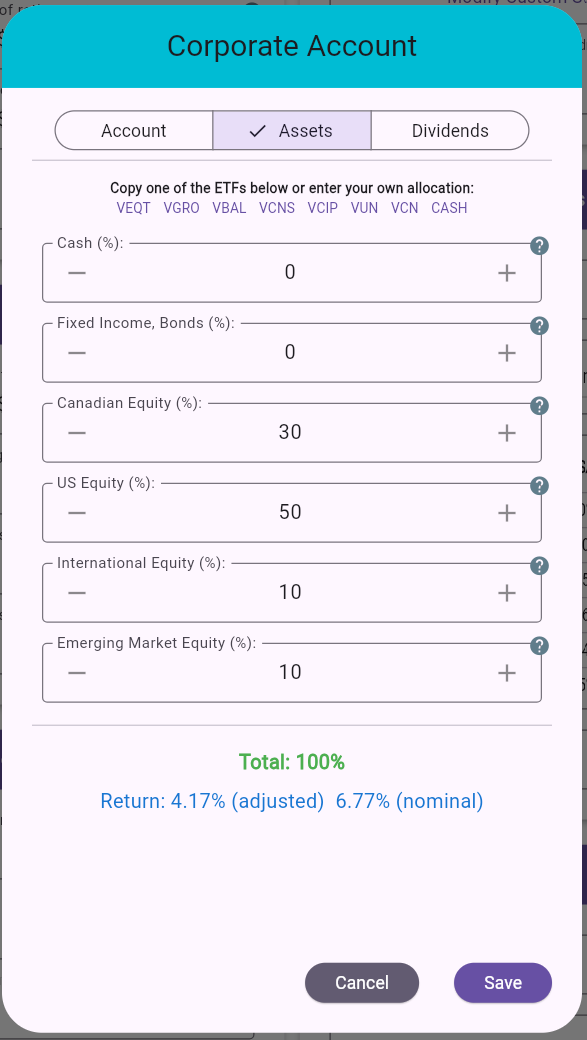

Figure 50: Corporate Account dialog - Assets tab

Asset allocation inputs Set corporate portfolio

mix across: Cash, Fixed Income/Bonds,

Canadian Equity, US Equity,

International Equity, and

Emerging Market Equity.

ETF shortcuts Quick presets for common ETF-style allocations.

Total % check Allocation must total 100%.

Implied return display Dialog shows implied adjusted/nominal return from the selected mix. In asset-allocation mode, MayRetire derives expected returns from asset-class assumptions (aligned with FP Canada projection guidelines), rather than asking you to enter a single return manually.

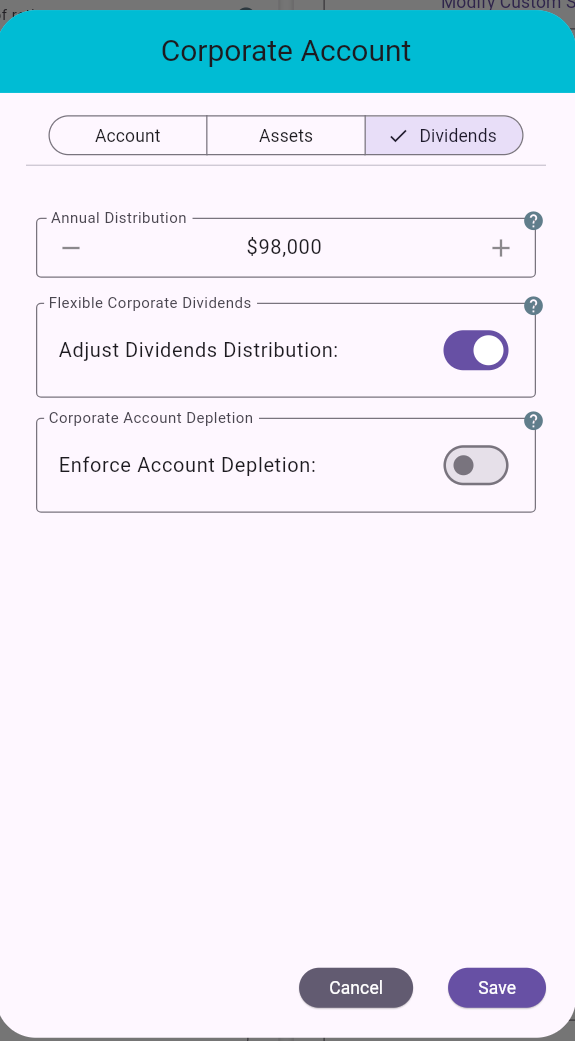

Figure 51: Corporate Account dialog - Dividends tab

Annual Distribution Base annual dividend amount to distribute from the corporation. MayRetire determines a tax-efficient composition of capital/eligible/non-eligible dividends for this payout.

Adjust Dividends Distribution When enabled, MayRetire adjusts annual corporate dividends to help bridge income needs (instead of using only a fixed dividend amount).

Enforce Account Depletion When enabled, MayRetire targets a payout path that fully depletes the corporate account by plan end.

MayRetire models corporate notional accounts to estimate how a CCPC investment portfolio may distribute cash during retirement. These balances are planning inputs and projections, not replacements for corporate tax records or professional tax filings.

Realized capital losses can reduce CDA and may create a negative CDA balance in the projection. A negative CDA must be offset by future CDA additions before tax-free capital dividends are available again.

NERDTOH is generally recovered when the corporation pays non-eligible dividends.

ERDTOH is generally recovered when the corporation pays eligible dividends. It can also be recovered through non-eligible dividend spillover when there is not enough GRIP to pay eligible dividends.

In MayRetire’s corporate investment-account model, GRIP is increased from eligible Canadian dividends received by the corporation. In real corporate tax planning, GRIP can also arise from other sources, such as active business income taxed at the general corporate rate. MayRetire does not currently model those additional GRIP-generating sources because this feature is intended for retirement planning with a CCPC investment portfolio, not for detailed operating-company tax planning.

When MayRetire distributes corporate cash, it uses a tax-aware dividend waterfall:

CDA first Positive CDA is paid first as tax-free capital dividends.

Eligible dividends next Eligible dividends are paid next, limited by available GRIP. These dividends reduce GRIP and recover ERDTOH where ERDTOH is available.

Non-eligible dividends after that Remaining required dividends are paid as non-eligible dividends. These recover NERDTOH first.

ERDTOH spillover If non-eligible dividends create more refund capacity than the remaining NERDTOH balance, the excess capacity can recover ERDTOH.

Refund sweep When dividend refunds create additional cash that can help meet the target distribution, MayRetire may sweep that refund out as additional non-eligible dividends. This uses the same NERDTOH-first, ERDTOH-spillover ordering.

MayRetire treats dividend refunds as part of the same annual corporate tax/refund settlement. In practice, a cash refund may be received after the corporation files its tax return, so exact cash timing can differ. For retirement projections, MayRetire applies the full refund in the current projection year as an annual net-tax simplification, similar to treating a tax refund as reducing the year’s overall tax drag.

Excess GRIP with no ERDTOH The corporation can still pay eligible dividends if GRIP is available. However, if ERDTOH is already zero, those eligible dividends do not generate an ERDTOH refund.

Excess ERDTOH with no or insufficient GRIP If GRIP is zero or too small, the corporation cannot pay enough eligible dividends to recover all ERDTOH directly. In that case, remaining ERDTOH may be recovered through non-eligible dividend spillover, after NERDTOH is recovered first.

GRIP and ERDTOH do not always move together in real life In MayRetire’s simplified CCPC investment-account model, eligible Canadian dividends tend to increase both GRIP and ERDTOH-related refundable tax. In real corporate tax planning, GRIP can increase without a matching ERDTOH increase. MayRetire’s model is designed to support retirement projections for corporate investment portfolios, not all operating-company tax scenarios.

Practical guidance:

Figure 52: Main planning action buttons - Calculate, Stress Test, Simulate, Backtest

These commands run your plan using different analysis methods. Use

them together: start fast with Calculate, challenge the

plan with Stress Test, validate robustness with

Simulate, then test real history with

Backtest.

Calculate Quick deterministic projection using a constant-return assumption. Best for rapid iteration while adjusting inputs. It does not model year-to-year market randomness.

Simulate Monte Carlo analysis (500 scenarios) that introduces return variability and sequence risk. Use this as the primary realism check after baseline setup. Confidence level reflects the share of scenarios where your plan remains sustainable for the full horizon. In many plans, a more flexible withdrawal approach and a less aggressive asset mix can improve simulation success rates.

Stress Test Runs a curated set of fixed adverse scenarios against your current asset-allocation plan. Unlike Monte Carlo, these scenarios are not random. Unlike Backtest, they are not tied to one exact historical period. They are intentionally severe and can be more conservative than many Monte Carlo outcomes. Stress Test is available only when using detailed asset allocation (not the simple overall-return method).

Backtest Runs your plan through historical market regimes instead of randomized scenarios. Useful for stress testing against known high-inflation and severe drawdown periods. A depletion event in a historical path highlights vulnerability to that return sequence.

Note: Each button’s Learn more link opens focused

guidance for interpreting that method’s outputs and limitations.

The top-right action bar provides quick access to navigation, file operations, sharing, and account actions.

Figure 53: Top Action Bar icon row including Suggested Adjustments

Scroll to the top Jumps to the top of the page.

Scroll to the bottom Jumps to the bottom of the page.

Open MayRetire GPT Opens the MayRetire GPT assistant.

Suggest adjustments Opens the Suggested Adjustments workflow for the current plan. Detailed workflow is covered in Suggest Adjustments.

Compare retirement plans Loads one or more

.json plan files and opens plan comparison. Detailed

workflow is covered in Compare Plans.

Check Survivor Safety Visible only when planning for a couple and both start/end ages cross the age-75 safety check window. Runs survivor safety analysis. Detailed workflow is covered in Check Survivor Safety.

Load retirement parameters from a file Loads saved plan parameters from file and resets current results.

Save retirement parameters to a file Prompts for a file name, then saves current plan parameters as JSON.

Save calculator screenshot to a file Prompts for a file name, then captures and saves a full-page screenshot.

Create PDF report Prompts for a file name, then generates and saves a PDF report.

Send feedback Opens feedback flow to contact support.

Open Facebook page Opens the MayRetire Facebook page.

Open subreddit Opens the MayRetire subreddit.

Open home page Redirects to the MayRetire home page.

Sign Out Shows a confirmation dialog. On confirm, clears current saved plan state and signs out.

Figure 54: Compare Retirement Plans dialog with metric chips and multi-plan chart

Use this dialog to compare multiple saved plan scenarios against each other and optionally against your currently loaded plan.

.json plan files. Typical usage

is 1 to 4 files.After Tax EstateLiquid AssetsNet IncomeCPP CollectedOAS CollectedDB CollectedAdd. Income CollectedCorp. Div. CollectedRRSP/RRIF/LIF BalanceTFSA BalanceUnreg. Acc. BalanceCorporate BalanceTotal Tax PaidEstate TaxPractical guidance:

CPP60, CPP65,

CPP70, etc.) so legend labels are immediately

meaningful.After Tax Estate, then review

Net Income and Total Tax Paid to understand

trade-offs.Zoom Y-Axis on for fine differences; turn it off

to evaluate absolute magnitude.

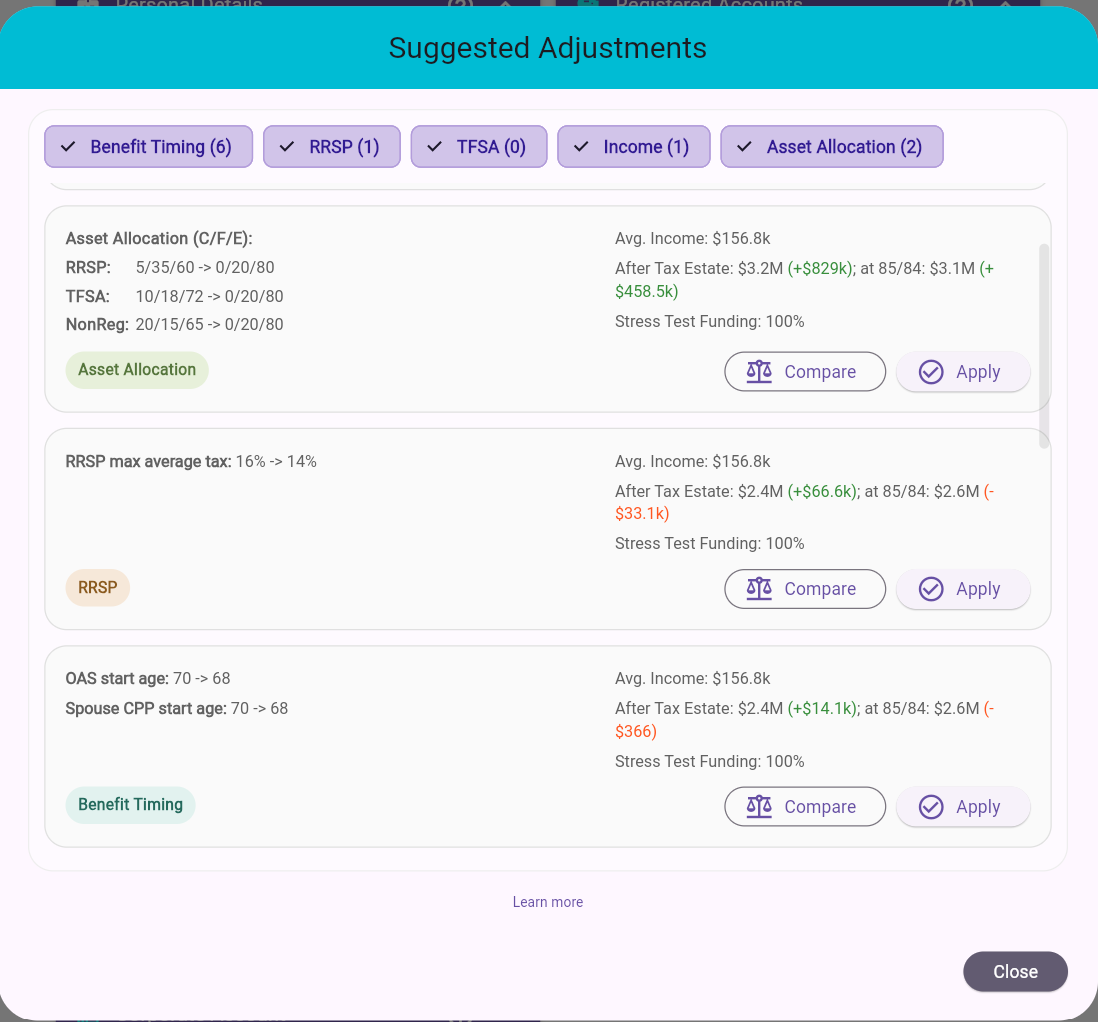

Figure 55: Suggested Adjustments dialog with category chips and adjustment cards

Suggested Adjustments helps surface a small set of potentially useful plan changes without running a full exhaustive optimization. This feature does not use AI to generate ideas. Instead, MayRetire evaluates targeted variations of your current plan and shows adjustments that appear promising enough to review.

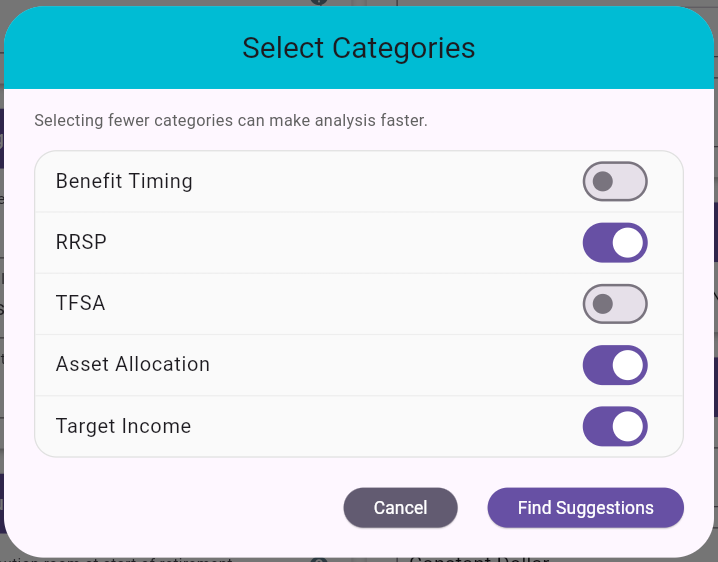

Figure 56: Select Categories dialog shown before generating suggestions

MayRetire opens Select Categories before generating suggestions so you can focus the search on the adjustment types you care about most.

Start the feature from the app’s Suggested Adjustments action.

MayRetire first opens Select Categories so you can choose which adjustment types to analyze.

After categories are chosen, MayRetire reviews the current plan and shows a progress dialog while generating possible adjustments.

If no suggestions are found for a narrowed category selection, MayRetire lets you reopen Select Categories and broaden the search.

If no suggestions are found even with all categories selected, MayRetire shows a simple no-adjustments message.

If suggestions are found, they are shown as cards inside the dialog.

Category chips at the top let you filter the list by suggestion type when multiple kinds of suggestions are present.

If not all categories were included in the search, the dialog also offers Select Categories so you can rerun with a different scope.

Compare

Apply

Yes, MayRetire opens Select

Categories again before rerunning the search.

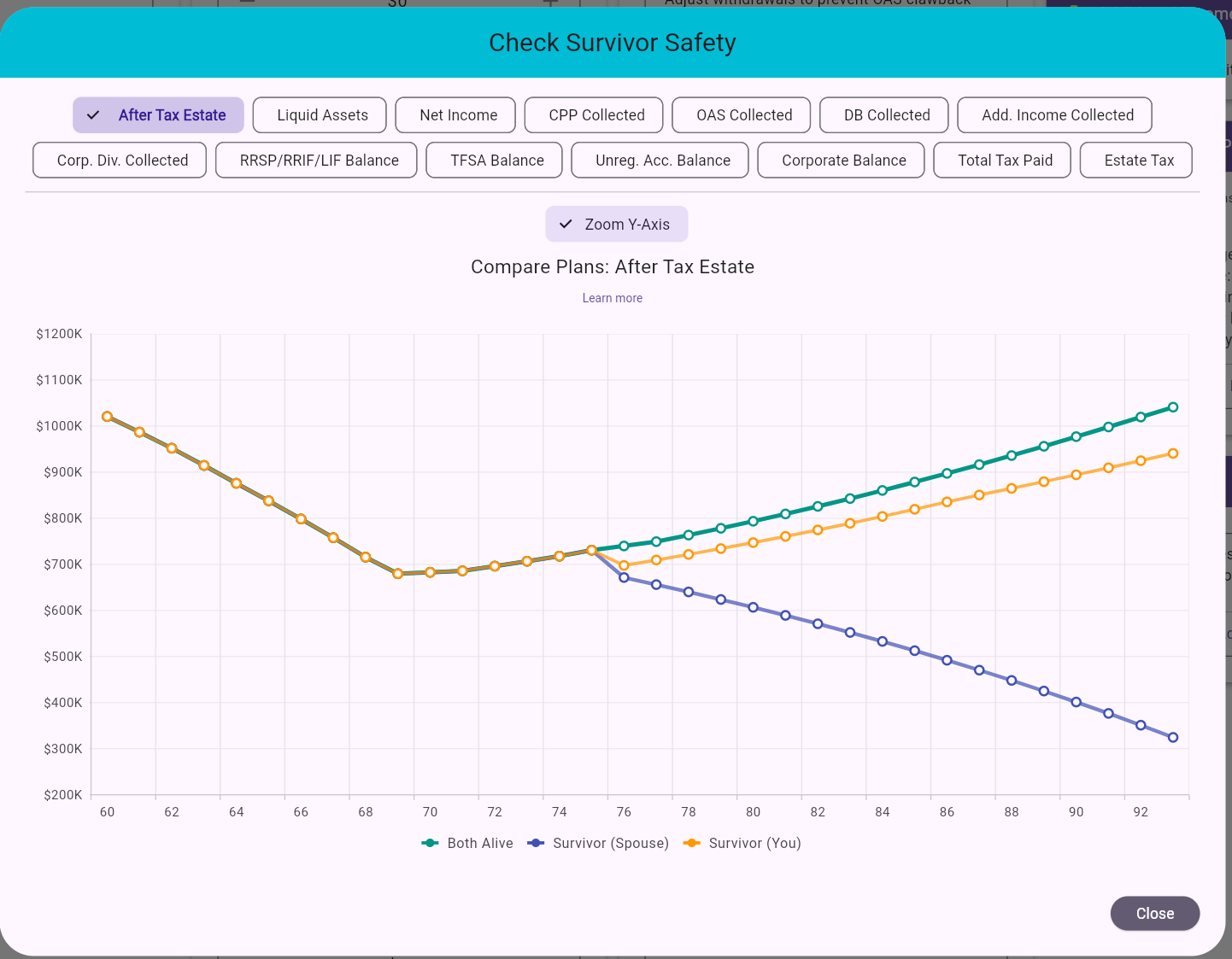

Figure 57: Check Survivor Safety dialog (Compare Plans framework with survivor scenarios)

This action reuses the Compare Plans charting framework, but instead of loading external files it auto-generates survivor scenarios to test household resilience.

Both Alive (base plan).Survivor (Spouse) (you pass away at age 75).Survivor (You) (spouse passes away at age 75).After Tax Estate, Liquid Assets,

Net Income, CPP Collected,

OAS Collected, DB Collected,

Add. Income Collected, Corp. Div. Collected,

RRSP/RRIF/LIF Balance, TFSA Balance,

Unreg. Acc. Balance, Corporate Balance,

Total Tax Paid, Estate Tax.Both Alive).Interpretation guidance:

Practical guidance:

After Tax Estate and Net Income

to confirm survivor sufficiency.This section documents the results area shown after running Calculate. The same results UI pattern is also reused in Stress Test, Simulate, and Backtest when you focus on a specific sequence or selected scenario.

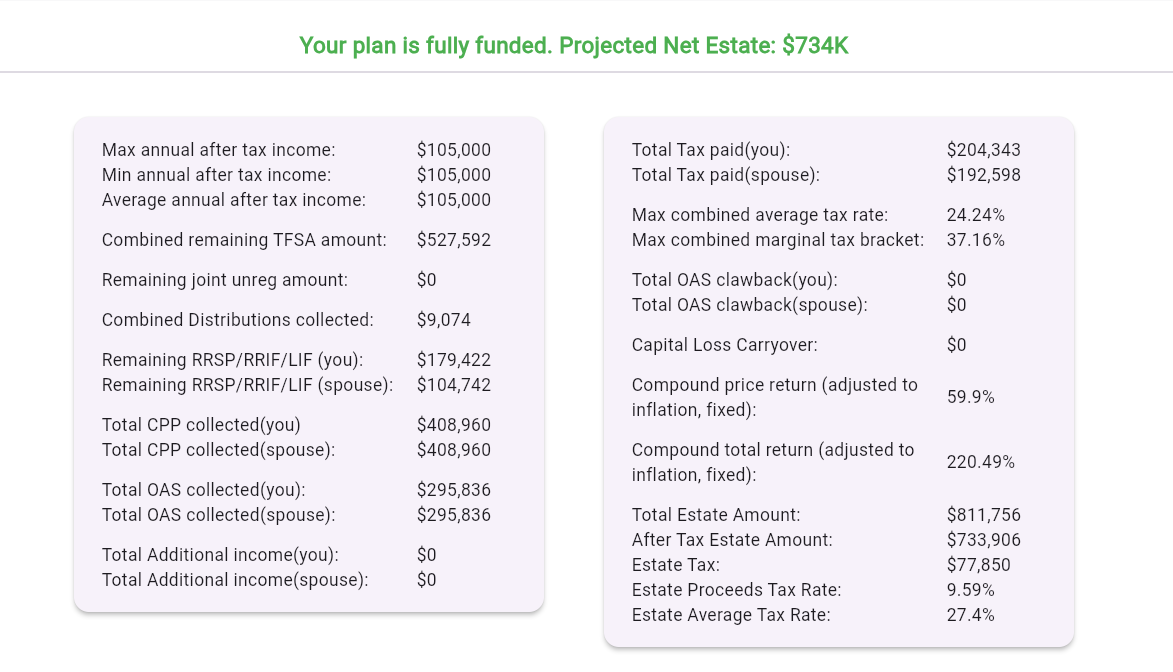

Figure 58: Fully funded outcome with projected net estate and summary cards

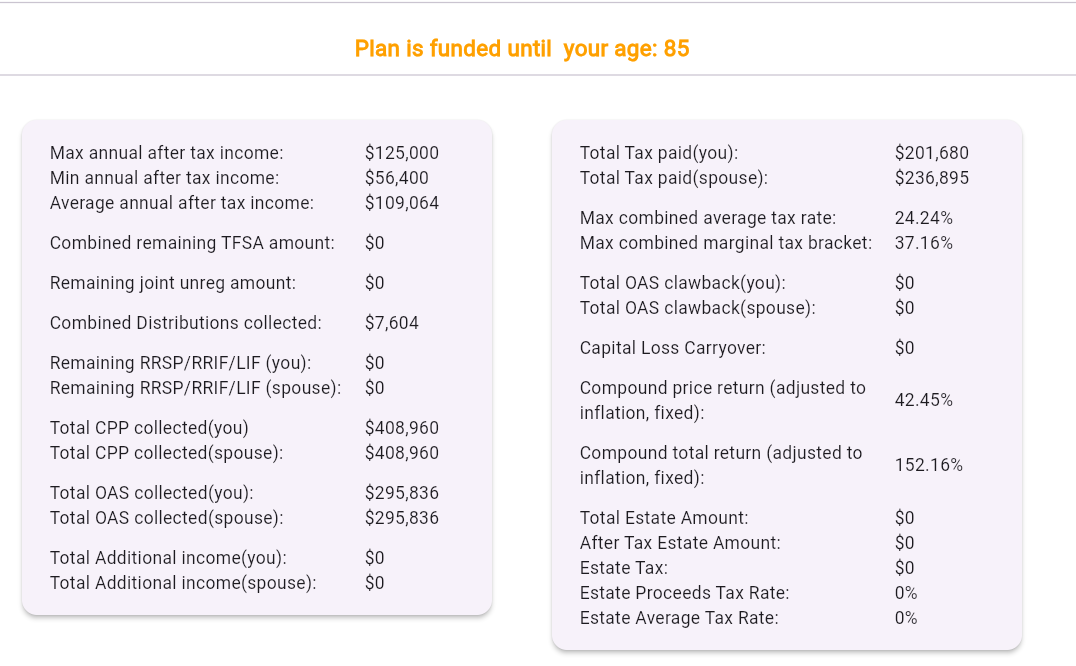

Figure 59: Partially funded outcome (funded until a specific age) with the same summary-card layout

The summary block provides a quick top-level diagnostic before you dive into charts or detailed yearly rows.

Left-side card (income/assets/benefits focus) includes:

Right-side card (tax/estate/returns focus) includes:

How to use this section effectively:

Min annual after tax income and

After Tax Estate Amount together to judge income stability

vs legacy outcome.This subsection will cover all results charts that appear below the

summary cards. Each chart will be documented in its own

sub-subsection (22.2.x) with:

Learn more guidance (when available).Charts show only relevant series MayRetire hides series that are not applicable to the current plan/scenario. Example: if no GIS is received in the plan, a GIS series will not be shown.

Toggle series from legend Click a legend item to show/hide that series. Use this to isolate one account, one spouse, or one metric line.

Hover for exact values Move the cursor over chart points to see detailed values for that specific year/age.

Collapse/expand chart sections Use the chart section chevron to collapse charts you are not using and expand them again when needed.

Use chart-specific Learn more links

Most charts include a Learn more action that explains

intent and interpretation nuances.

Read trends, not only endpoints Two plans can finish similarly but differ substantially in mid-retirement stress years.

Use complementary views Charts, summary cards, and the detailed projections table present the same plan through different lenses: trend view, headline metrics, and year-by-year detail.

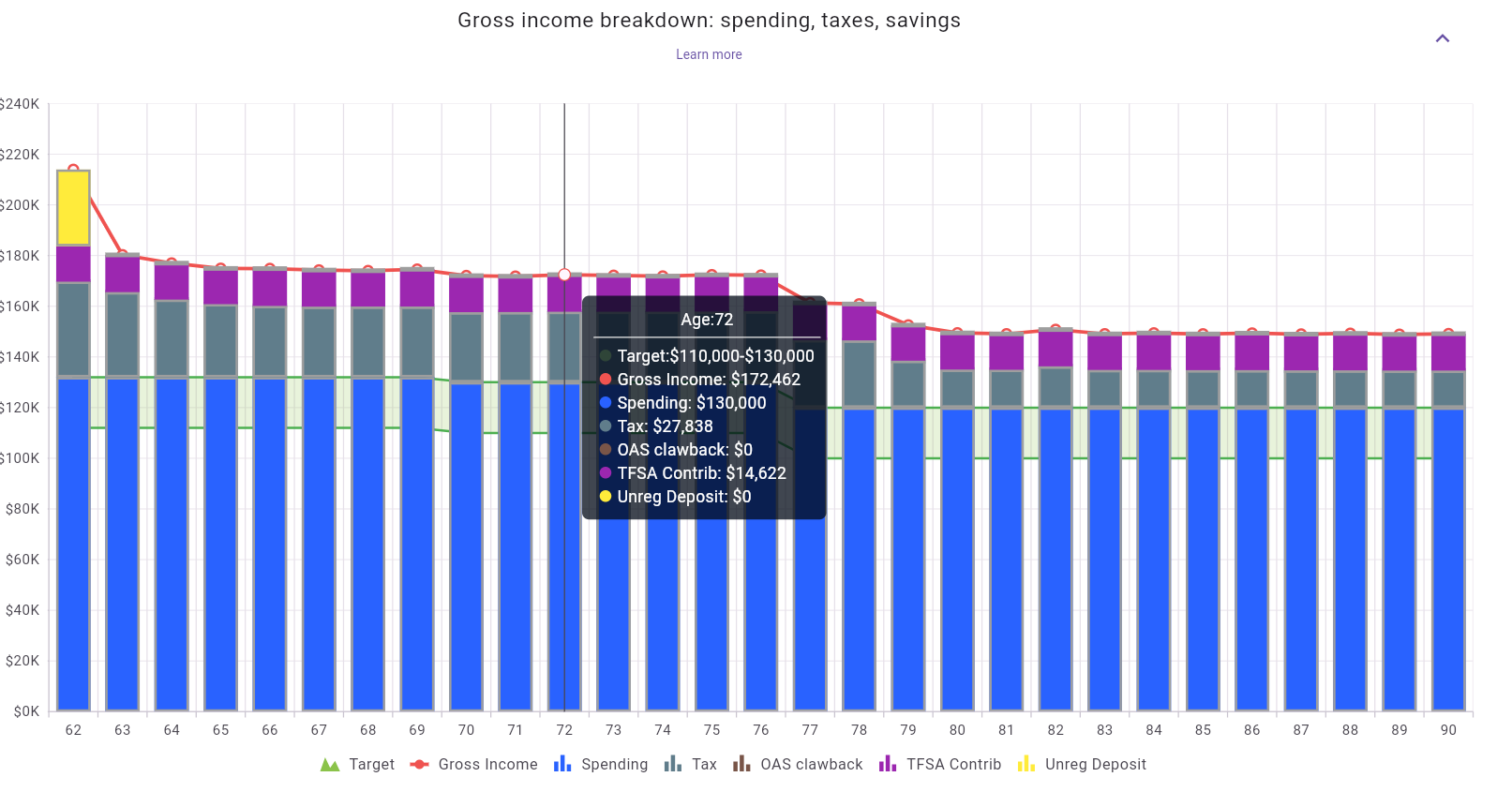

Figure 60: Gross income breakdown chart (spending, taxes, OAS clawback, savings)

What this chart shows:

How to read it:

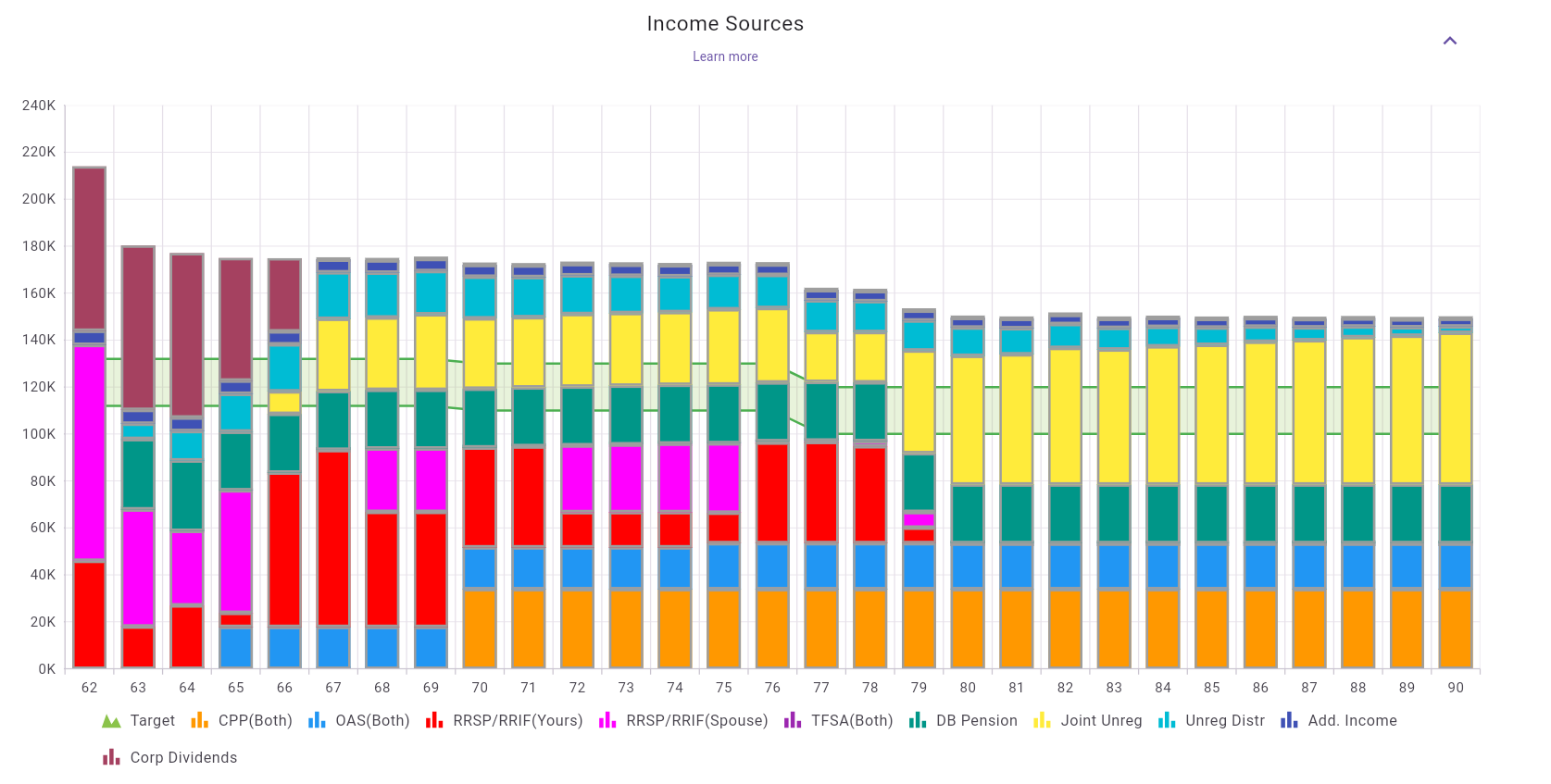

Figure 61: Income Sources chart (stacked annual income by source plus target line)

What this chart shows:

How to read it:

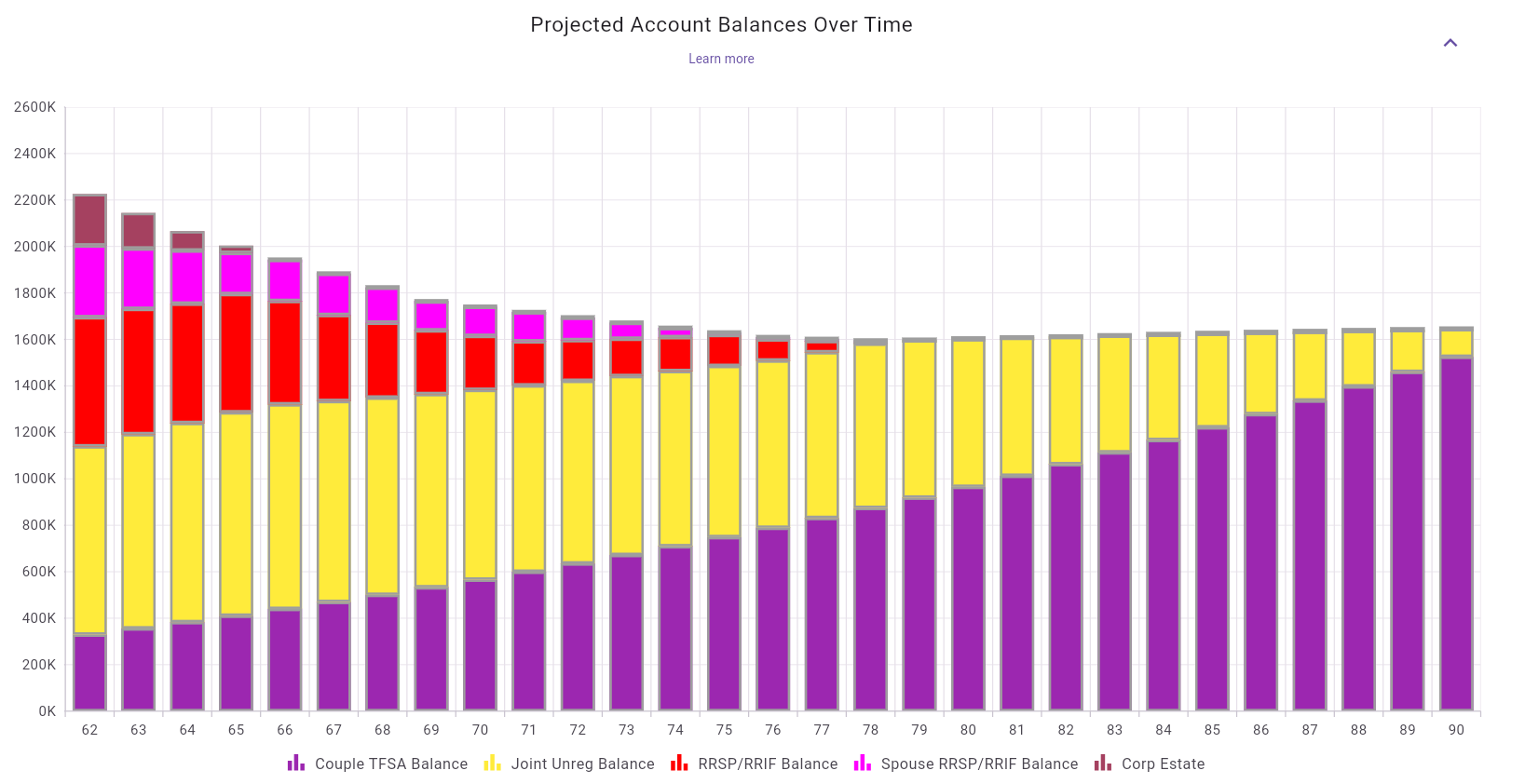

Figure 62: Projected account balances over time (stacked by account type)

What this chart shows:

How to read it:

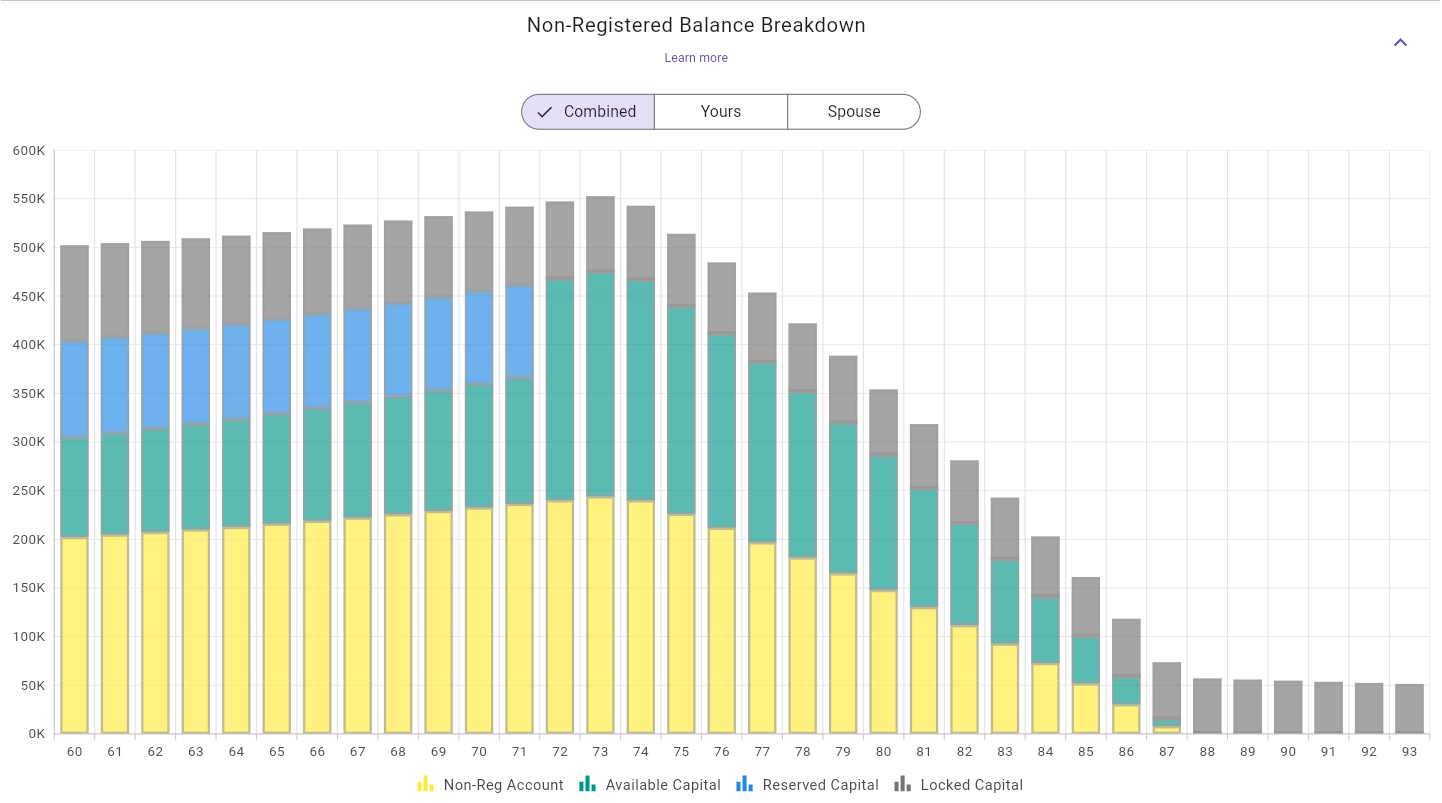

This chart appears when the plan includes investment portfolios. It provides a more detailed view of taxable non-registered assets than the overall account-balance chart.

Figure 63: Non-registered balance breakdown by account and portfolio capital access

What this chart shows:

Non-Reg Account balance.Available CapitalReserved CapitalLocked CapitalCombined, Yours, and Spouse.How to read it:

Combined to understand total taxable non-registered

wealth.Yours and Spouse to inspect

attribution and survivor-sensitive ownership patterns.Interpretation guidance:

This chart block is available for couple plans, where cross-spouse taxable attribution and splitting effects can be shown.

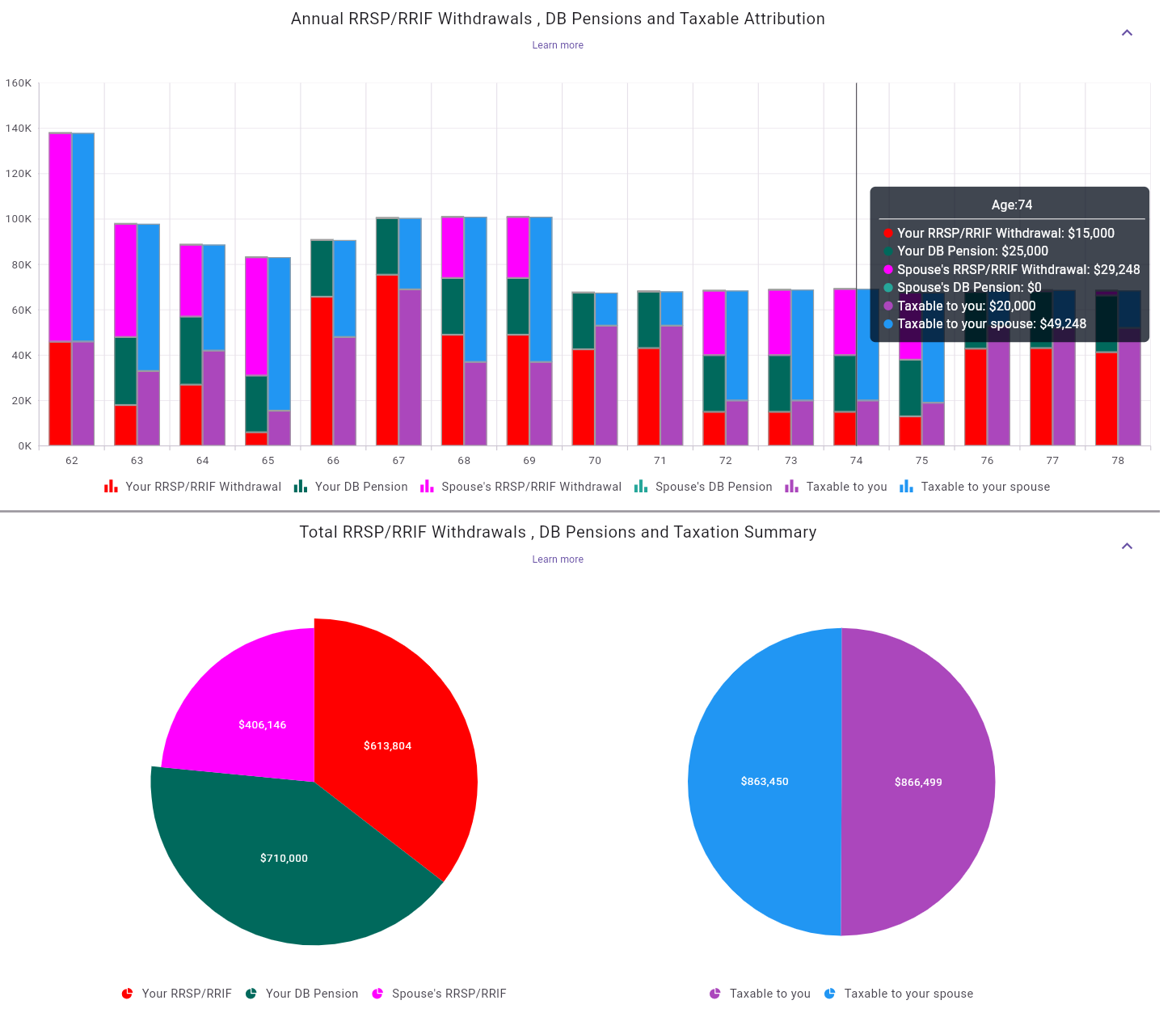

Figure 64: Annual attribution chart (top) and total-withdrawal/taxation summary pies (bottom)

What this chart block shows:

How to read it:

Interpretation note for this example:

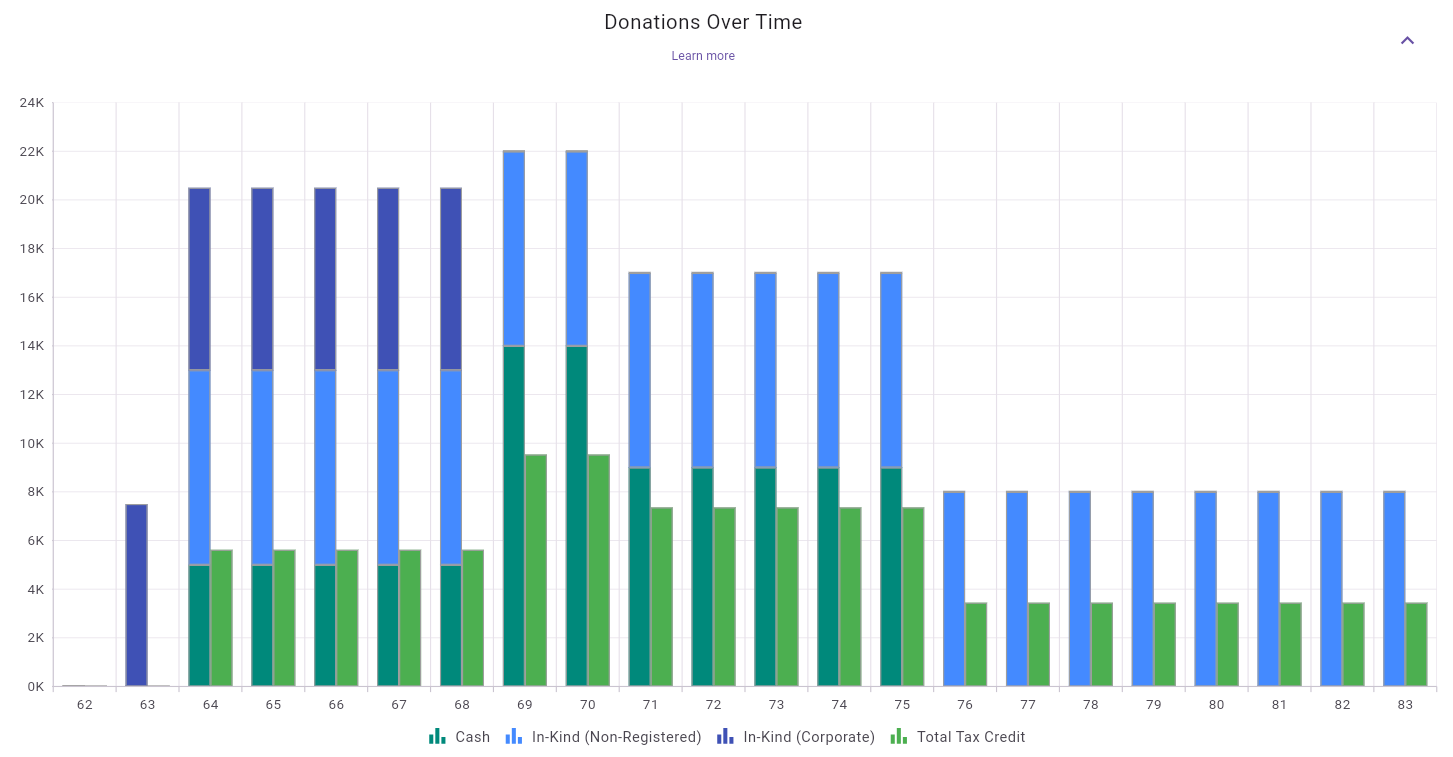

This chart appears only when at least one donation is configured in the plan.

Figure 65: Donations chart with stacked funding types and total tax credit

What this chart shows:

CashIn-Kind (Non-Registered)In-Kind (Corporate) when applicableTotal Tax Credit series when the plan includes personal

donations that generate donation tax credits.How to read it:

Interpretation guidance:

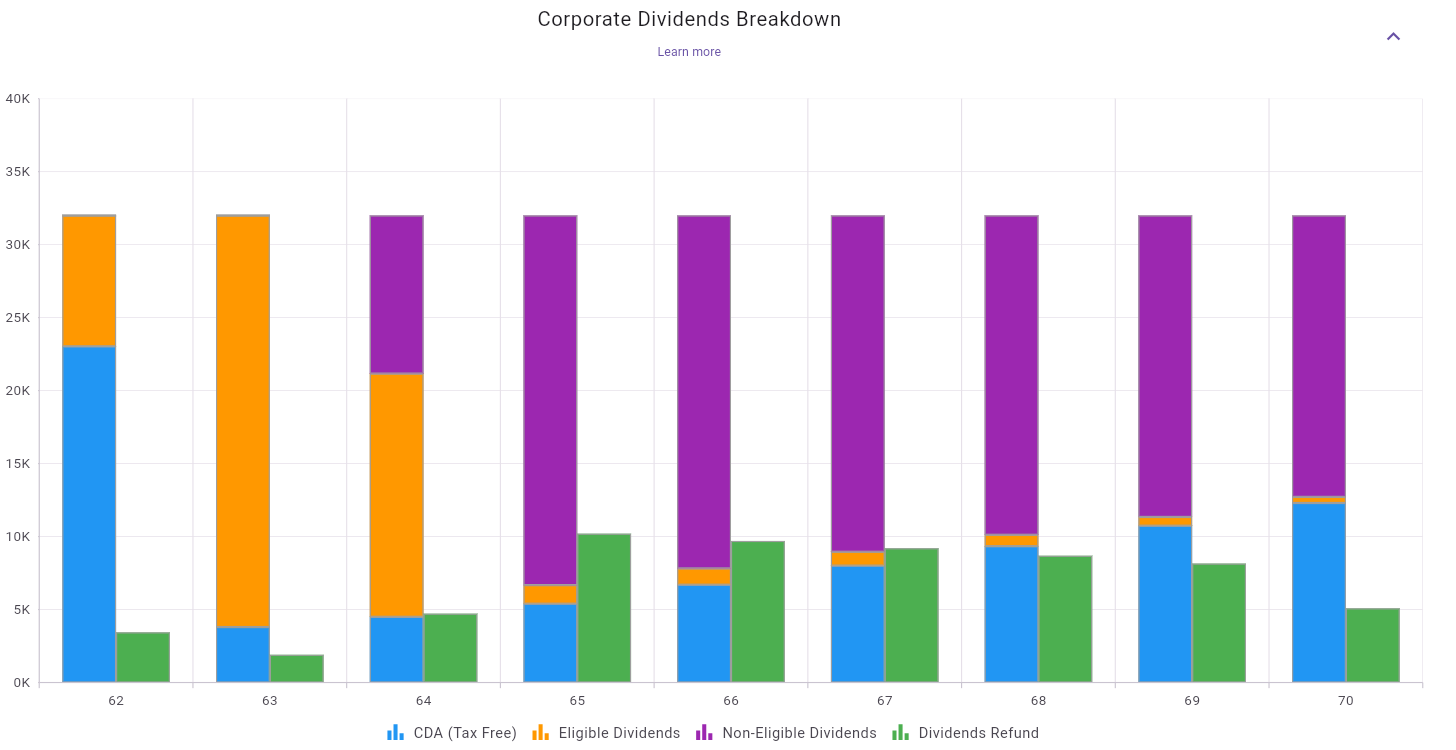

Figure 66: Corporate dividends composition and refundable-tax flow over time

What this chart shows:

CDA (Tax Free)Eligible DividendsNon-Eligible DividendsDividends Refund series showing refundable-tax recovery

flow (RDTOH refund effect).How to read it:

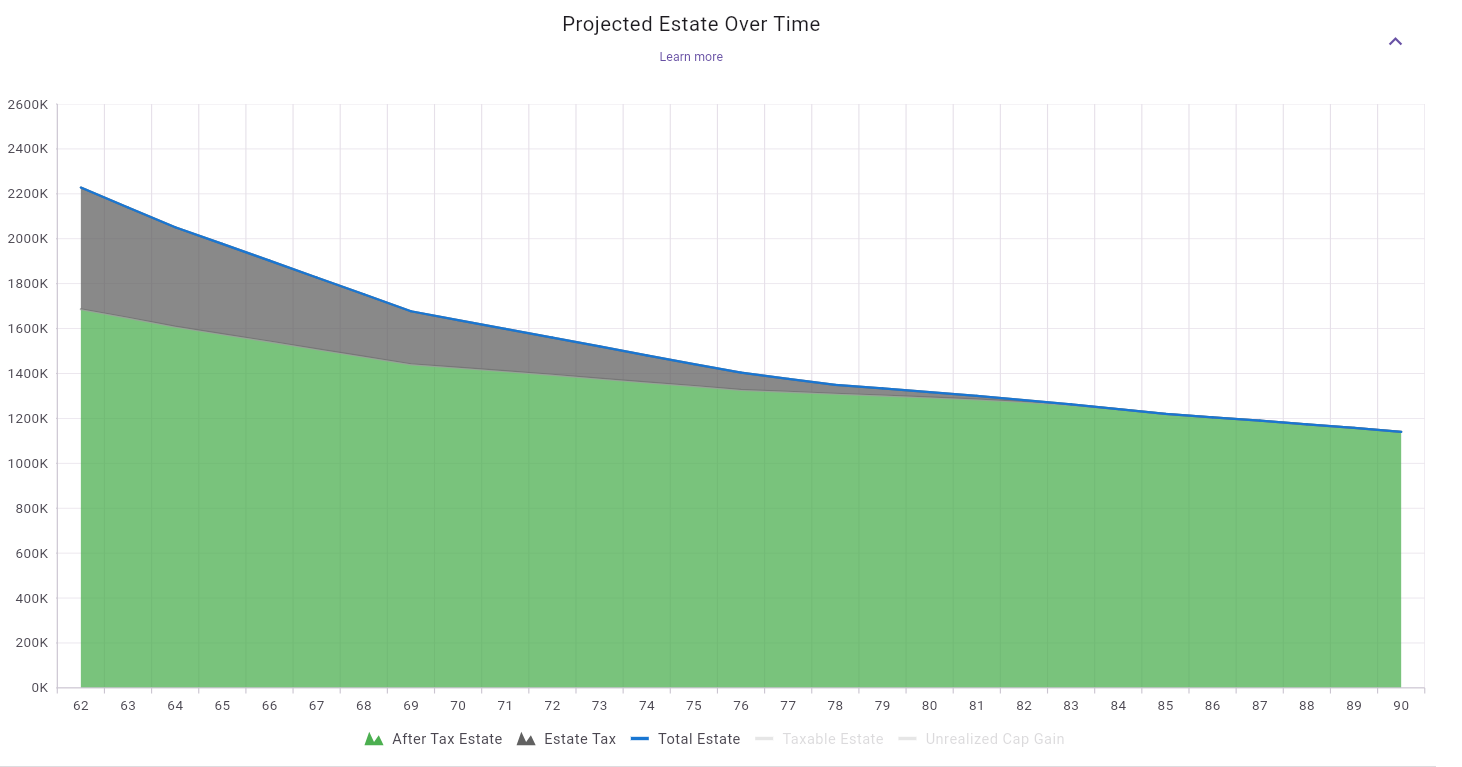

Figure 67: Projected estate over time (total, after-tax, and estate-tax components)

What this chart shows:

After Tax EstateEstate TaxTotal EstateHow to read it:

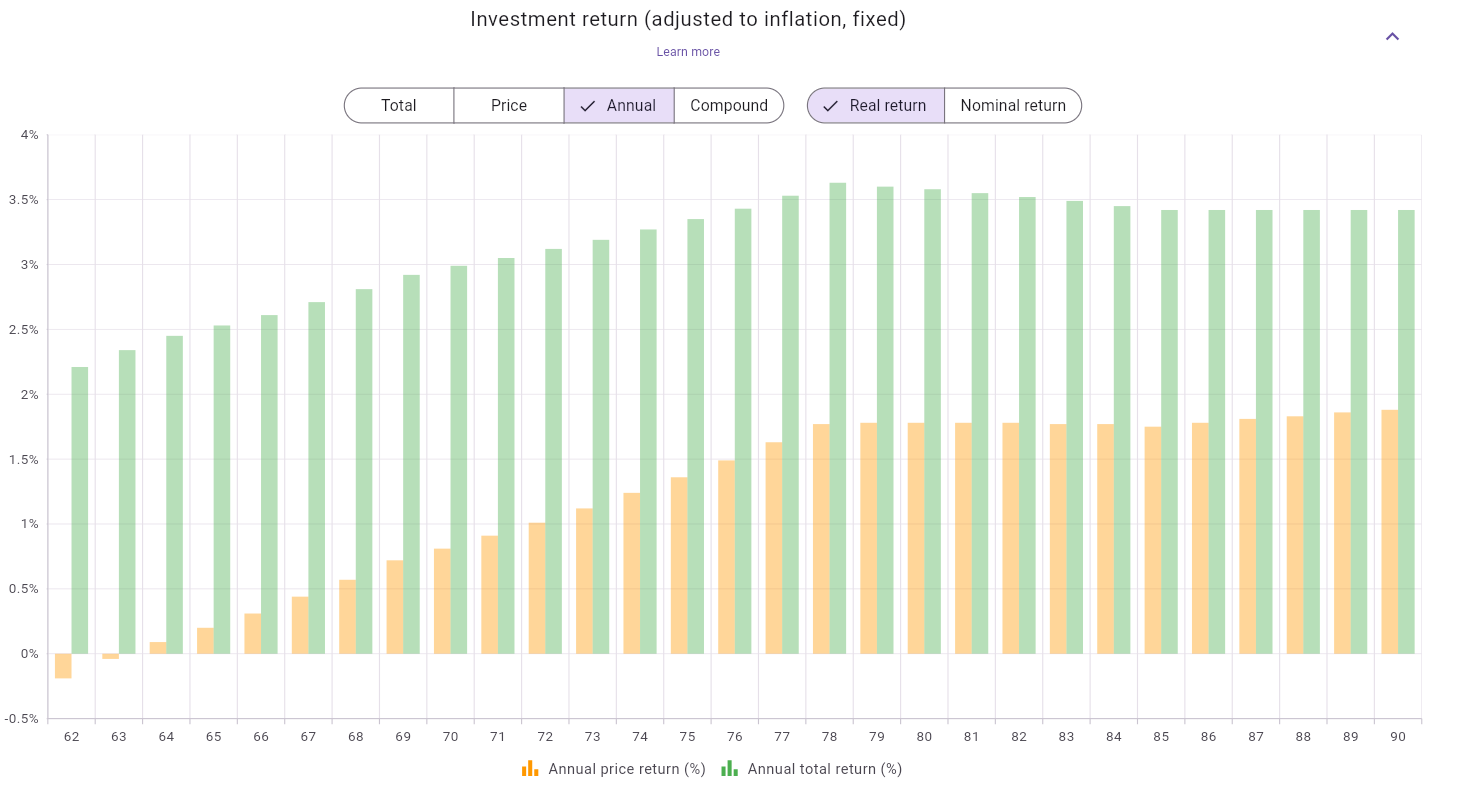

Figure 68: Investment return chart in Annual + Real-return view

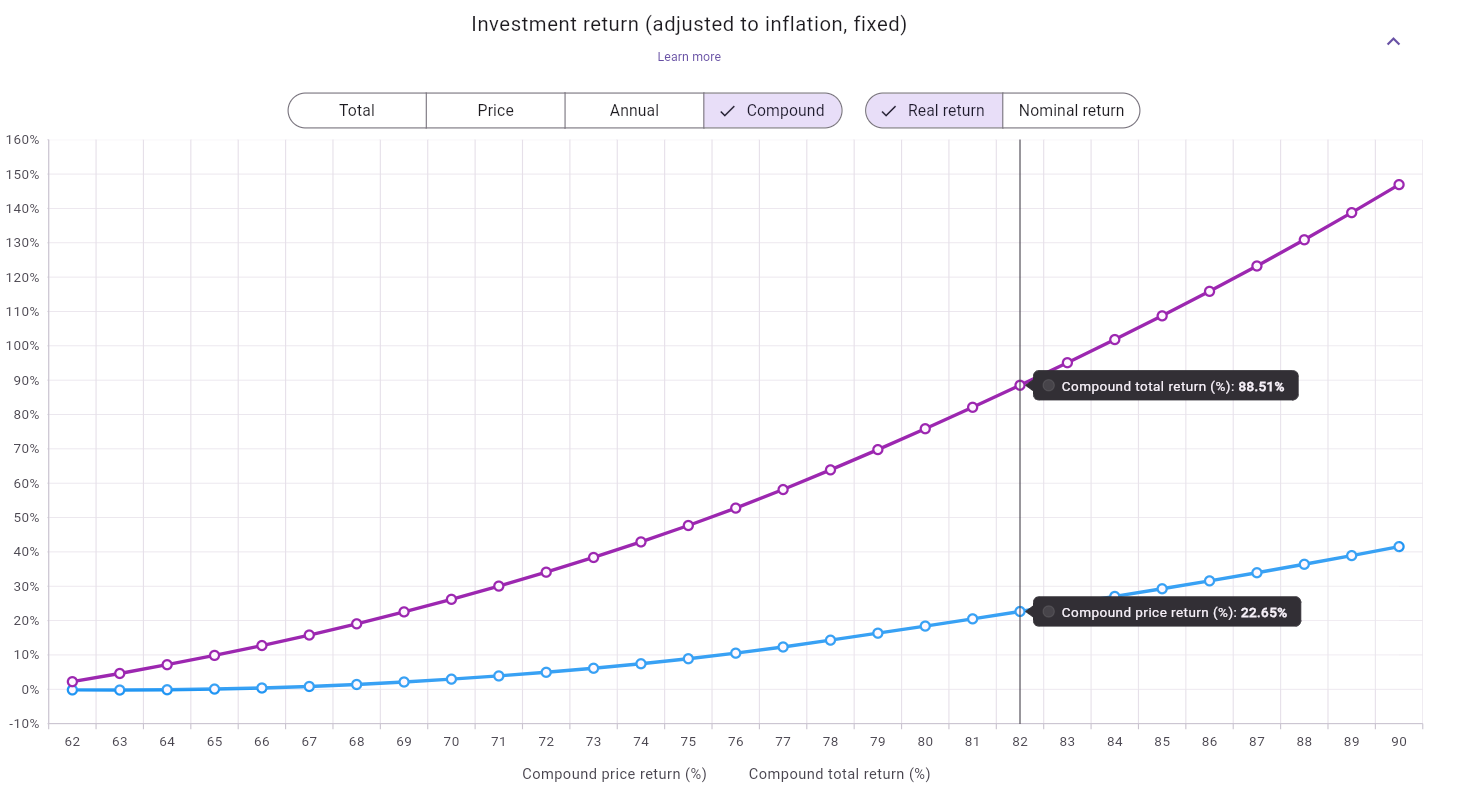

Figure 69: Investment return chart in Compound + Real-return view

What this chart shows:

Total or

PriceAnnual or

CompoundReal return

(inflation-adjusted) or Nominal returnHow to read the two views shown:

Interpretation guidance:

Price vs Total to understand the

role of distributions/dividends in overall growth.

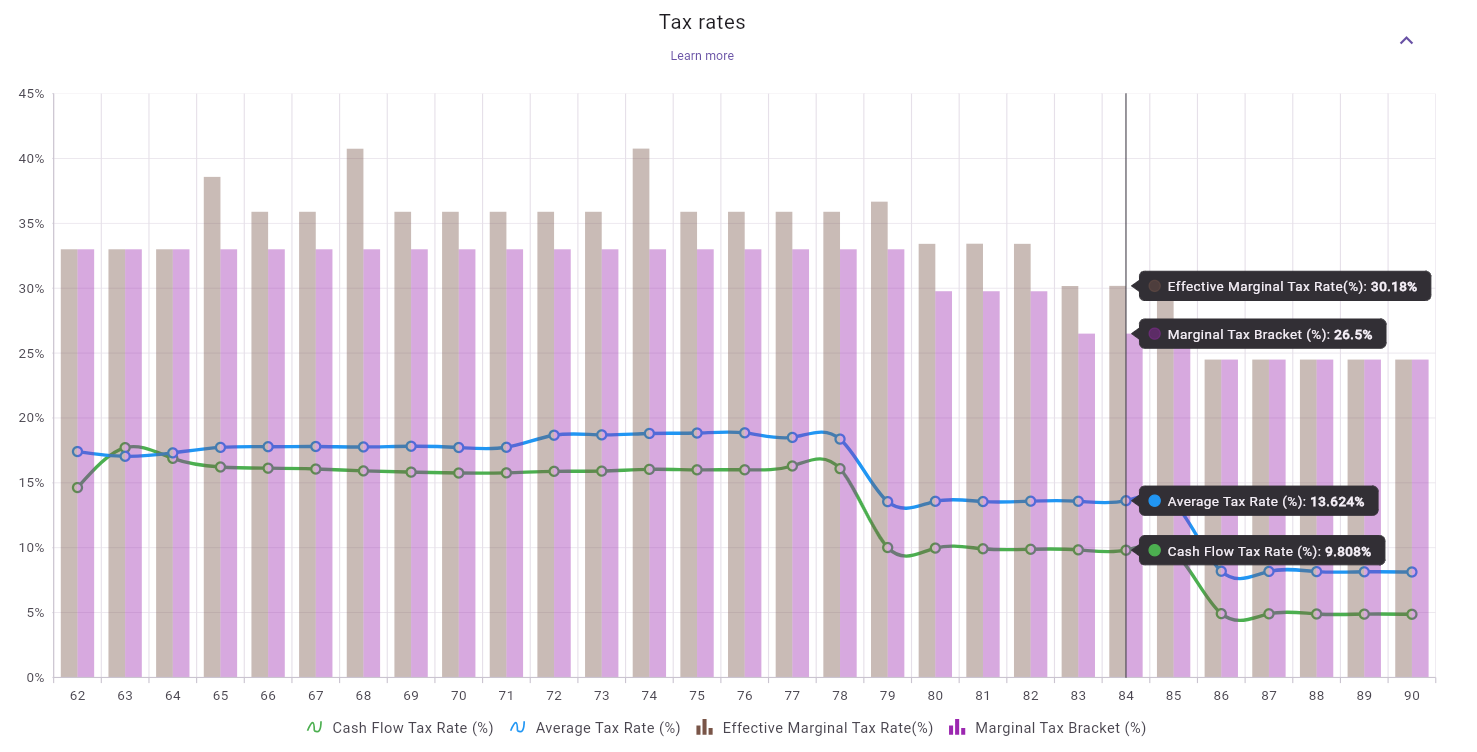

Figure 70: Tax rates chart (cash-flow, average, effective marginal, and bracket rates)

What this chart shows:

Cash Flow Tax Rate (%)Average Tax Rate (%)Effective Marginal Tax Rate (%)Marginal Tax Bracket (%)How to read it:

Interpretation guidance:

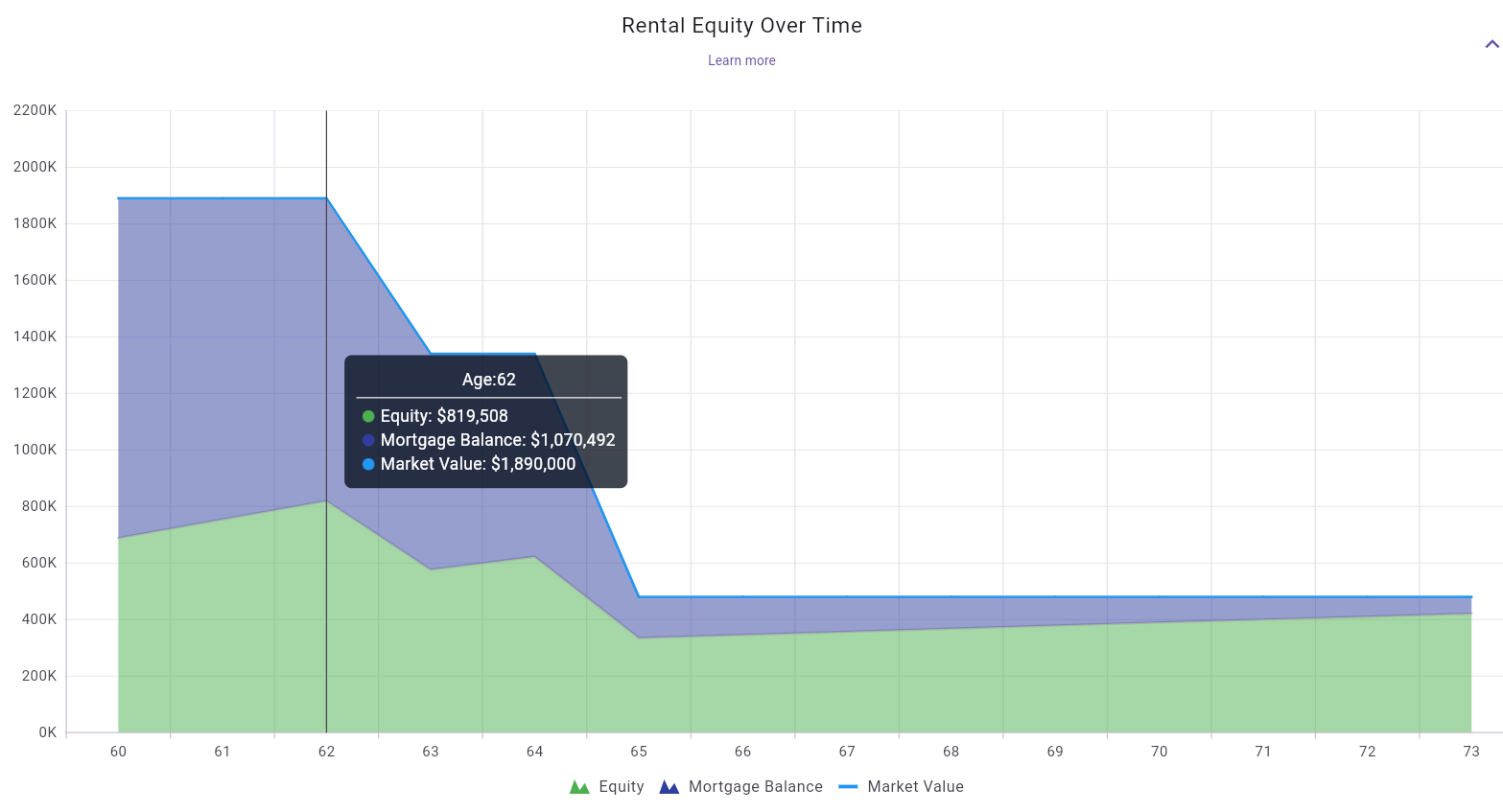

This chart appears only when at least one rental property is configured in the plan.

Figure 71: Rental equity chart (market value, mortgage balance, and resulting equity)

What this chart shows:

Market ValueMortgage BalanceEquityHow to read it:

Interpretation guidance:

This chart appears only when at least one rental property is configured in the plan.

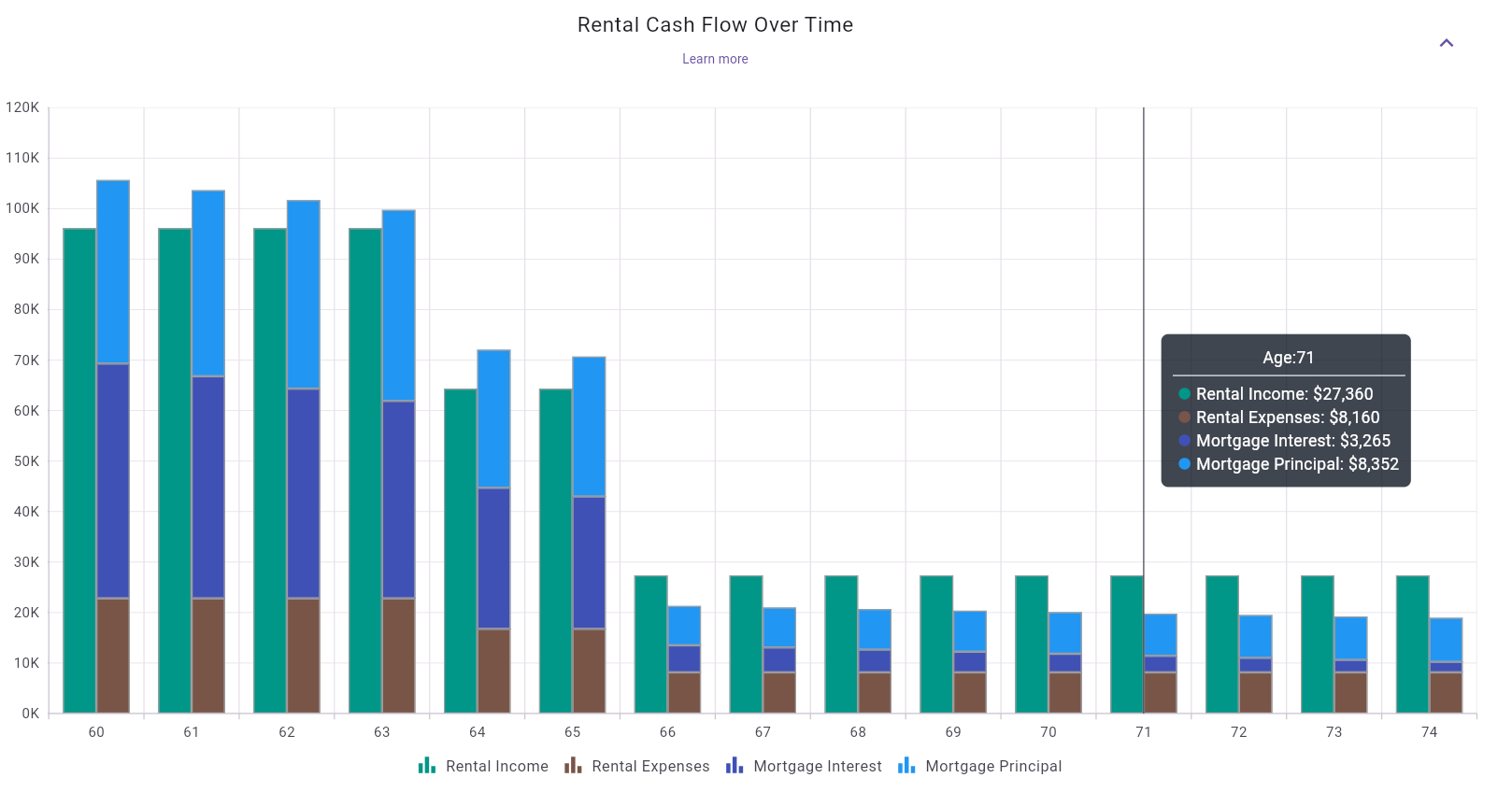

Figure 72: Rental cash-flow chart (income, expenses, mortgage interest, and mortgage principal)

What this chart shows:

Rental IncomeRental ExpensesMortgage InterestMortgage PrincipalHow to read it:

Interpretation guidance:

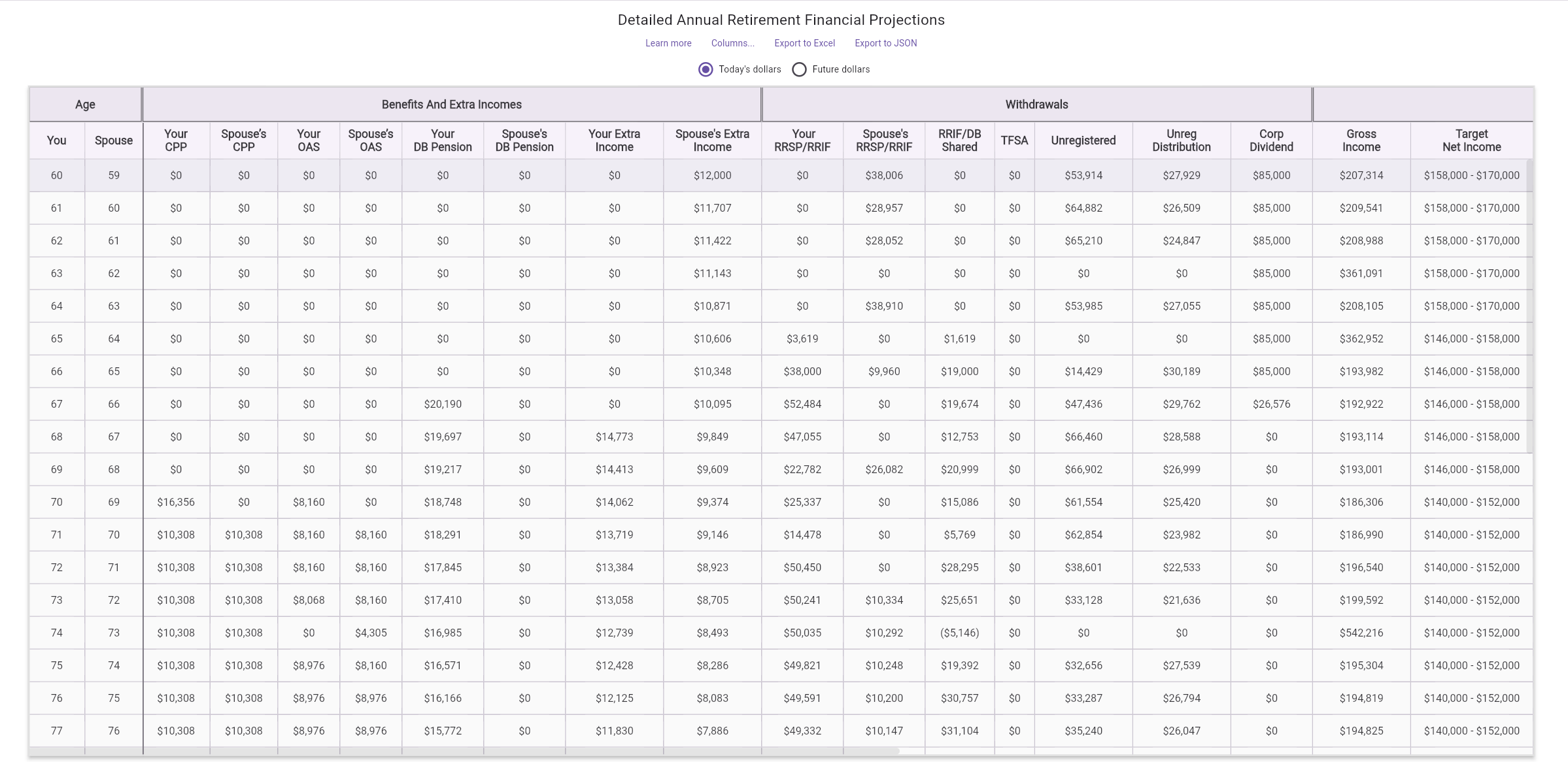

The detailed table is the year-by-year numeric companion to the summary cards and charts. It lets you inspect exact values for each age and each major planning component.

Figure 73: Detailed annual retirement financial projections table with grouped columns and top actions

What this section shows:

Top actions above the table:

Columns...: open the column-group picker to simplify

the view.Export to Excel: download the projections for

spreadsheet analysis and sharing.Export to JSON: download structured projection data for

integrations or custom analysis.Today's dollars / Future dollars: switch

display basis to inflation-adjusted or nominal-dollar views.Usage tips:

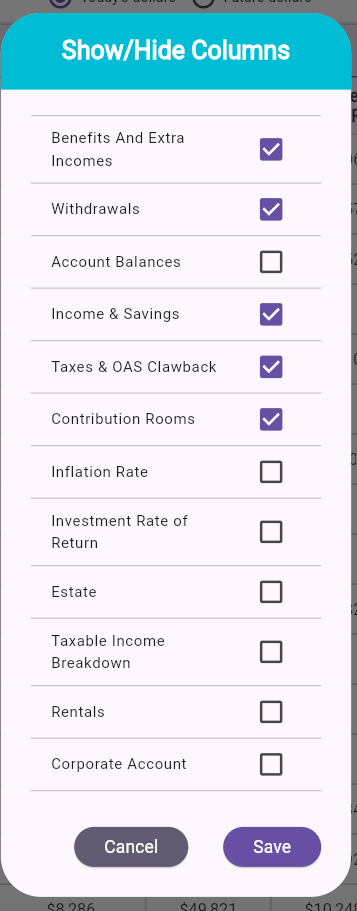

Figure 74: Show/Hide Columns dialog for selecting table column groups

What this dialog does:

Typical workflow:

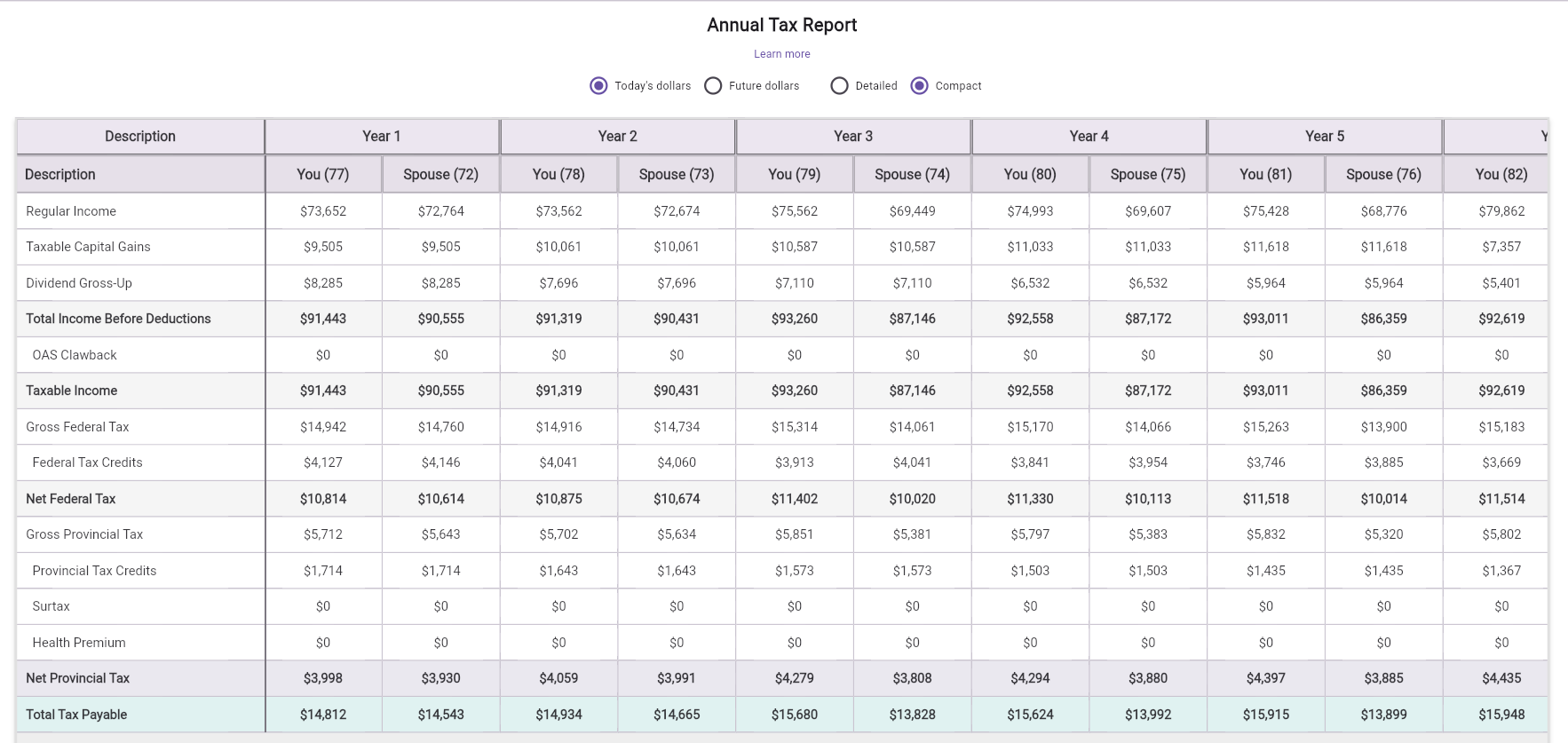

The Annual Tax Report is a worksheet-style companion to the detailed projections table. It focuses on tax computation rather than account balances or withdrawal mechanics, making it easier to review deductions, credits, surtax, health premium, and total tax payable across the retirement timeline.

Figure 75: Annual tax report with year-grouped columns, per-person values, and detailed or compact tax views

What this section shows:

You and

Spouse while both are alive.Age: N.Controls above the table:

Learn more: opens contextual help for interpreting the

report.Today's dollars / Future dollars: changes

only the tax report display basis, independently from the detailed

projections table.Detailed / Compact: switches between a

fuller tax audit view and a shorter summary view.Export to Excel: downloads the currently selected tax

report view for spreadsheet review, using the chosen

Today's dollars / Future dollars basis and

Compact, Standard, or Detailed

mode.What the rows cover:

Total Tax Payable.Usage tips:

Detailed when validating how credits and add-ons

affect tax.Compact when scanning many years side by side.MayRetire can evaluate multiple RRSP/RRIF withdrawal strategies for the currently selected return sequence and show the outcome tradeoffs side by side.

Figure 76: Entry link to evaluate RRSP withdrawal strategies for the active sequence

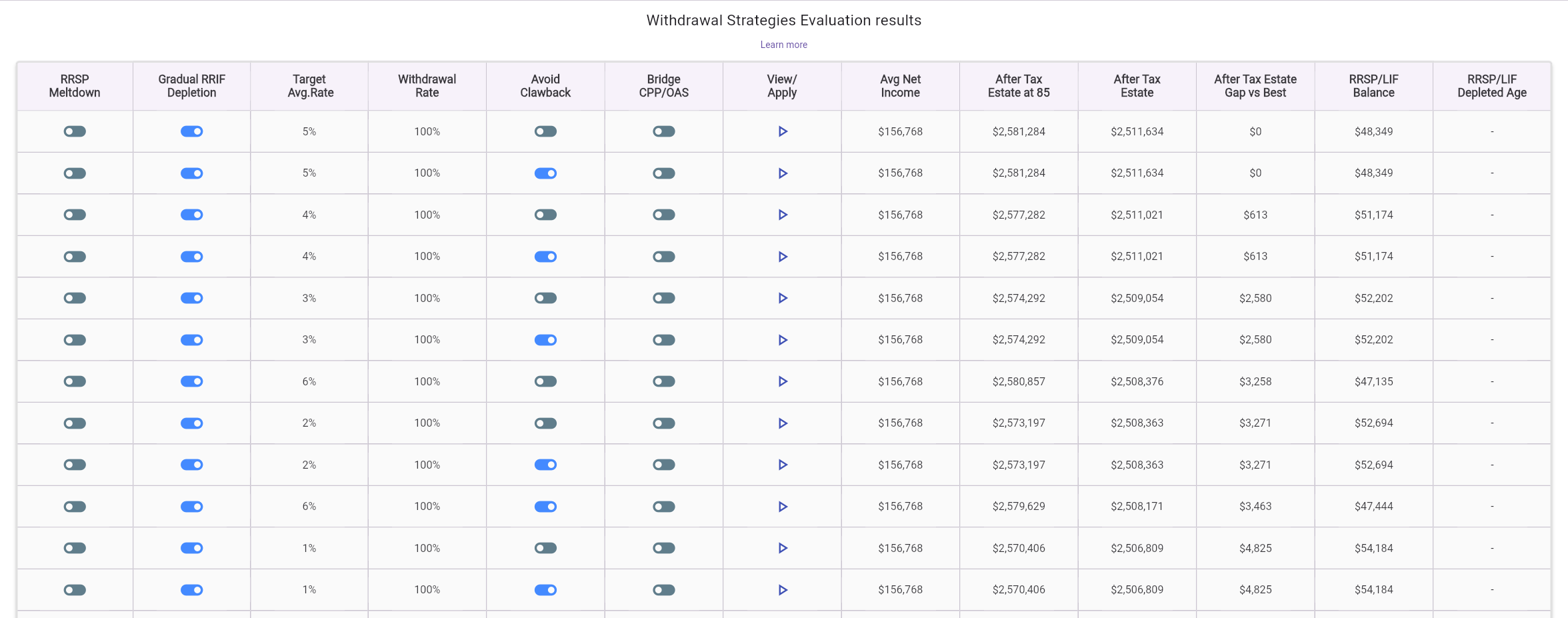

Figure 77: Withdrawal strategy evaluation table with strategy settings and key outcome metrics

How it works:

Evaluate different withdrawal strategies for this sequence of returns.View/Apply on any row to load that strategy and

immediately inspect its full output in charts and the detailed annual

projections table for the same sequence.What the evaluation table includes:

RRSP Meltdown,

Gradual RRIF Depletion, target average tax rate, withdrawal

rate, OAS-clawback handling, and CPP/OAS bridge options).When to use it:

Stress Test runs a small curated set of fixed adverse market regimes and shows how your plan behaves under each one. The goal is not to estimate probability. The goal is to pressure-test the plan against a handful of deliberately difficult environments that are easy to interpret and compare.

Figure 78: Stress Test outcomes with scenario tiles, baseline reference, and selected scenario focus

What this view shows:

Baseline tile

for normal assumptions.How the summary is calculated:

75%.Baseline tile is shown for reference but is

not included in the average stress score.How to read the tiles:

Fully funded plus Net Estate, orFunded: xx% plus the age reached.How to use it:

Baseline tile to

see how much deterioration the stress path causes.Interpretation guidance:

These scenarios are stylized planning tests, not forecasts. They were chosen to represent adverse regimes that retirement-income research repeatedly identifies as dangerous:

The scenario set is informed by retirement-income research and practitioner commentary from sources such as:

What it represents:

Why it matters:

Why it was selected:

What it represents:

Why it matters:

Why it was selected:

What it represents:

Why it matters:

Why it was selected:

What it represents:

Why it matters:

Why it was selected:

What it represents:

Why it matters:

Why it was selected:

What it represents:

Why it matters:

Why it was selected:

Practical guidance across all scenarios:

The Simulate run summarizes retirement sustainability across 500 randomized return scenarios, then surfaces key risk/opportunity patterns.

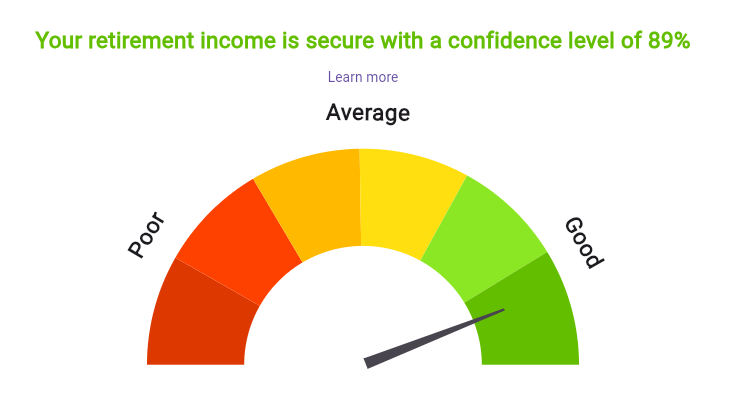

Figure 79: Simulation confidence-level gauge (success-rate summary)

What this view shows:

89%)

indicating the share of simulation paths where retirement income

remained sustainable through the plan horizon.How to read it:

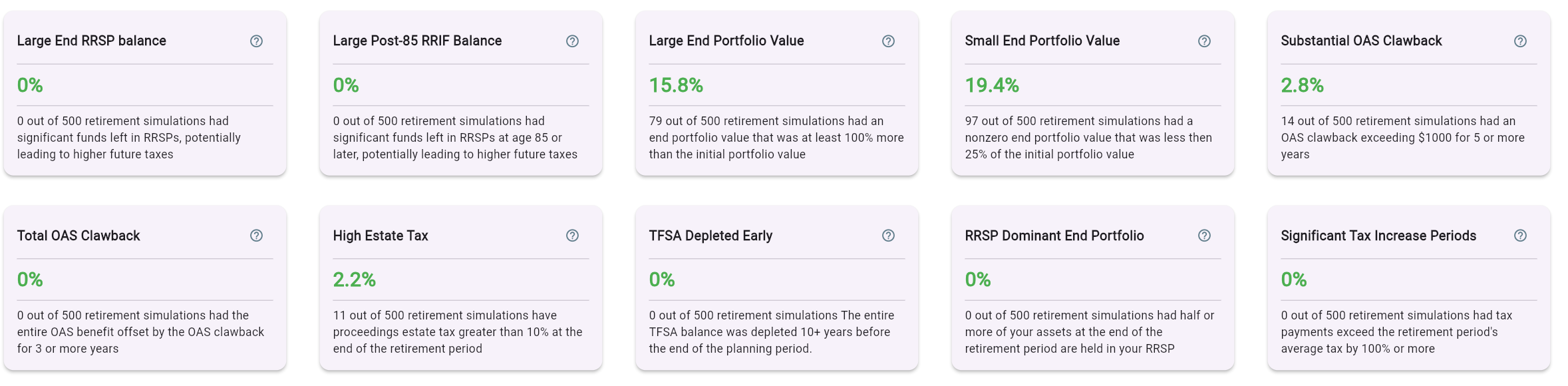

Figure 80: Simulation highlights cards (frequency of important risk and outcome patterns)

What this view shows:

Large End Portfolio ValueSmall End Portfolio ValueSubstantial OAS ClawbackHigh Estate TaxTFSA Depleted EarlyRRSP Dominant End PortfolioHow to use it:

These charts provide distribution-aware views of simulation outcomes across age, instead of a single deterministic path.

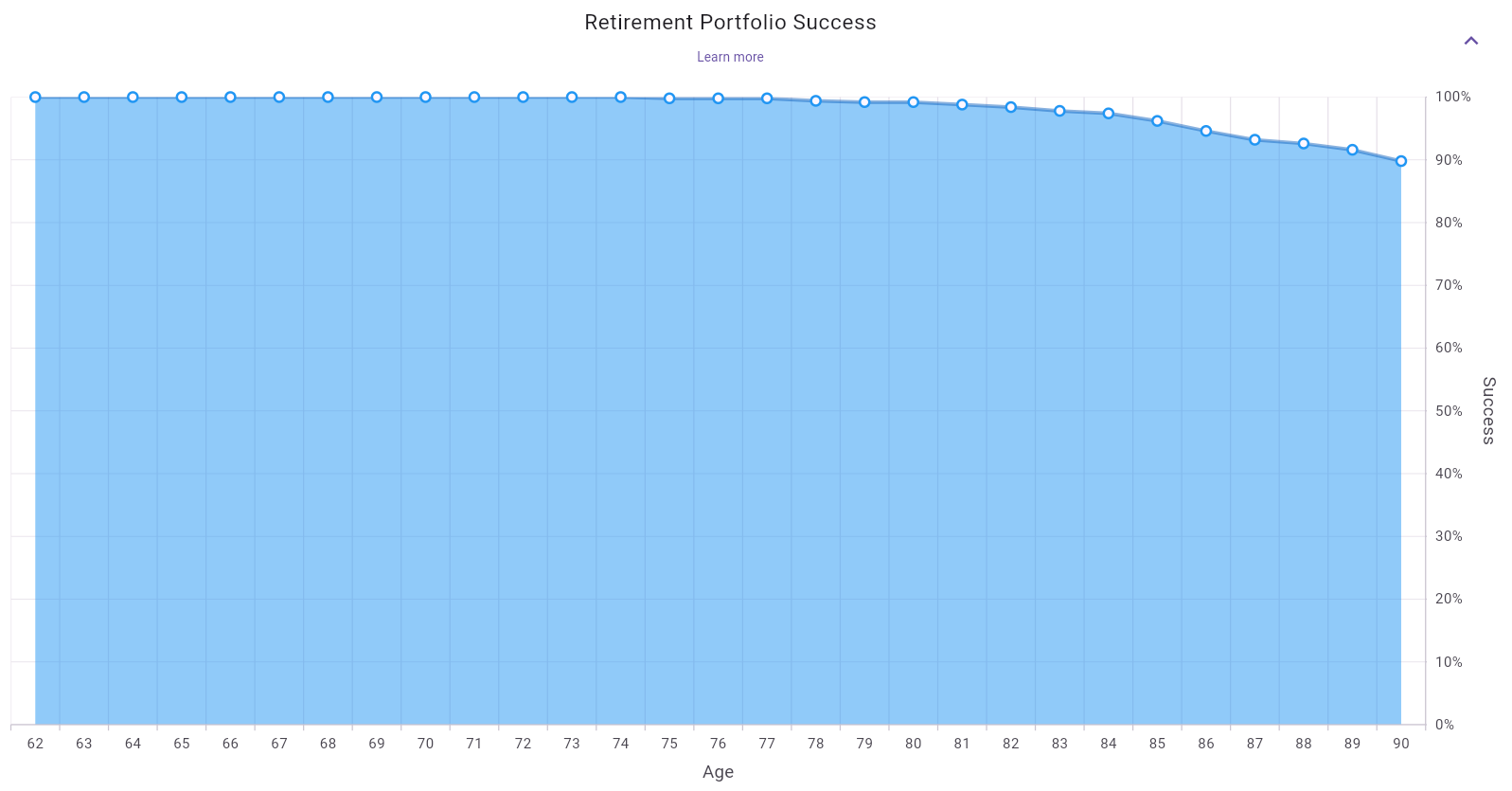

Figure 81: Retirement portfolio success curve by age under Monte Carlo simulation

What this chart shows:

How to read it:

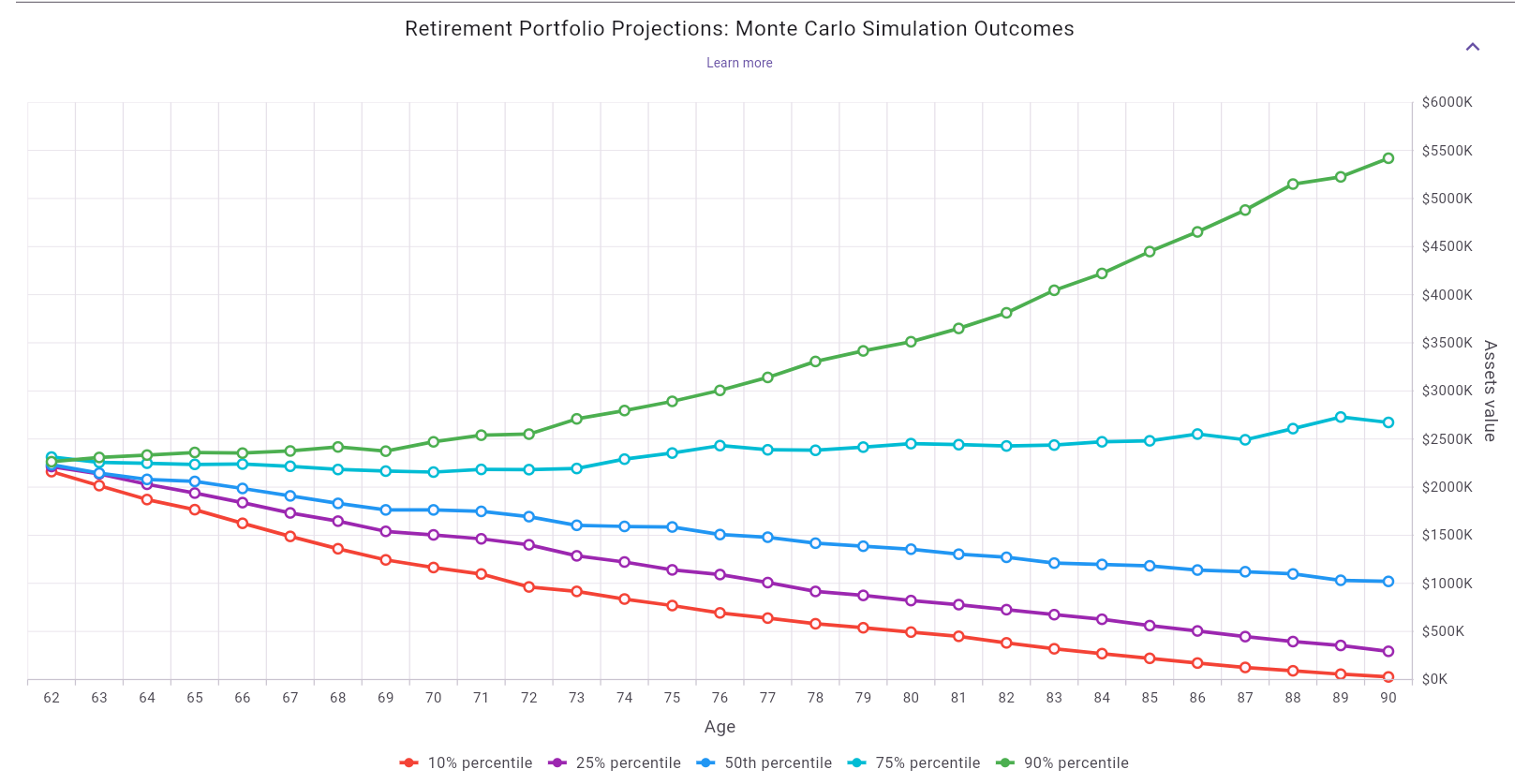

Figure 82: Monte Carlo portfolio outcomes with percentile paths (10th, 25th, 50th, 75th, 90th)

What this chart shows:

10th percentile (stress path)25th percentile50th percentile (median)75th percentile90th percentile (strong path)What “percentile” means (plain language):

10th percentile means 10% of simulations were at or

below that value (and 90% were above it).50th percentile means the median outcome: half of

simulations were below and half were above.90th percentile means only 10% of simulations were

above that value.How to read it:

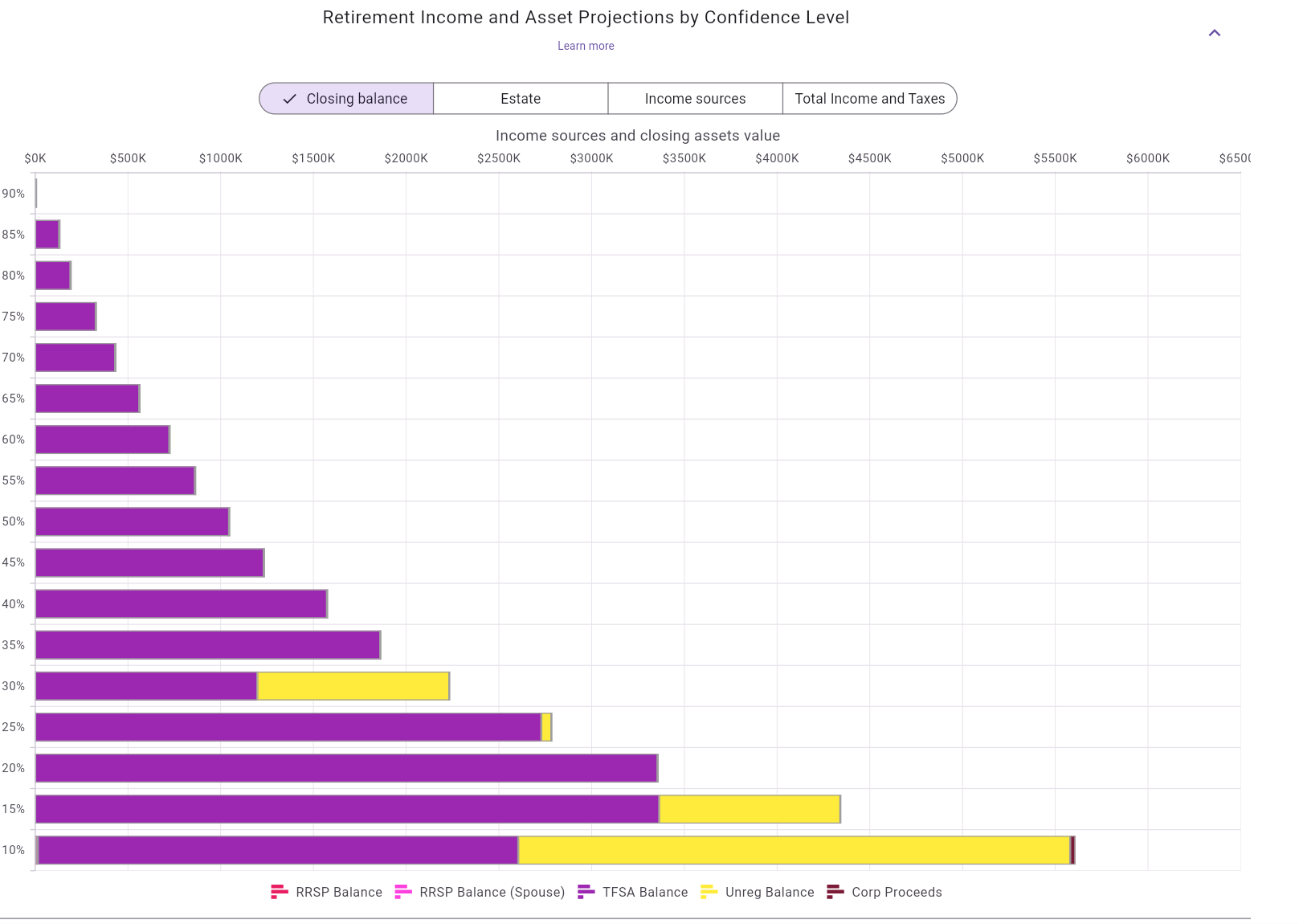

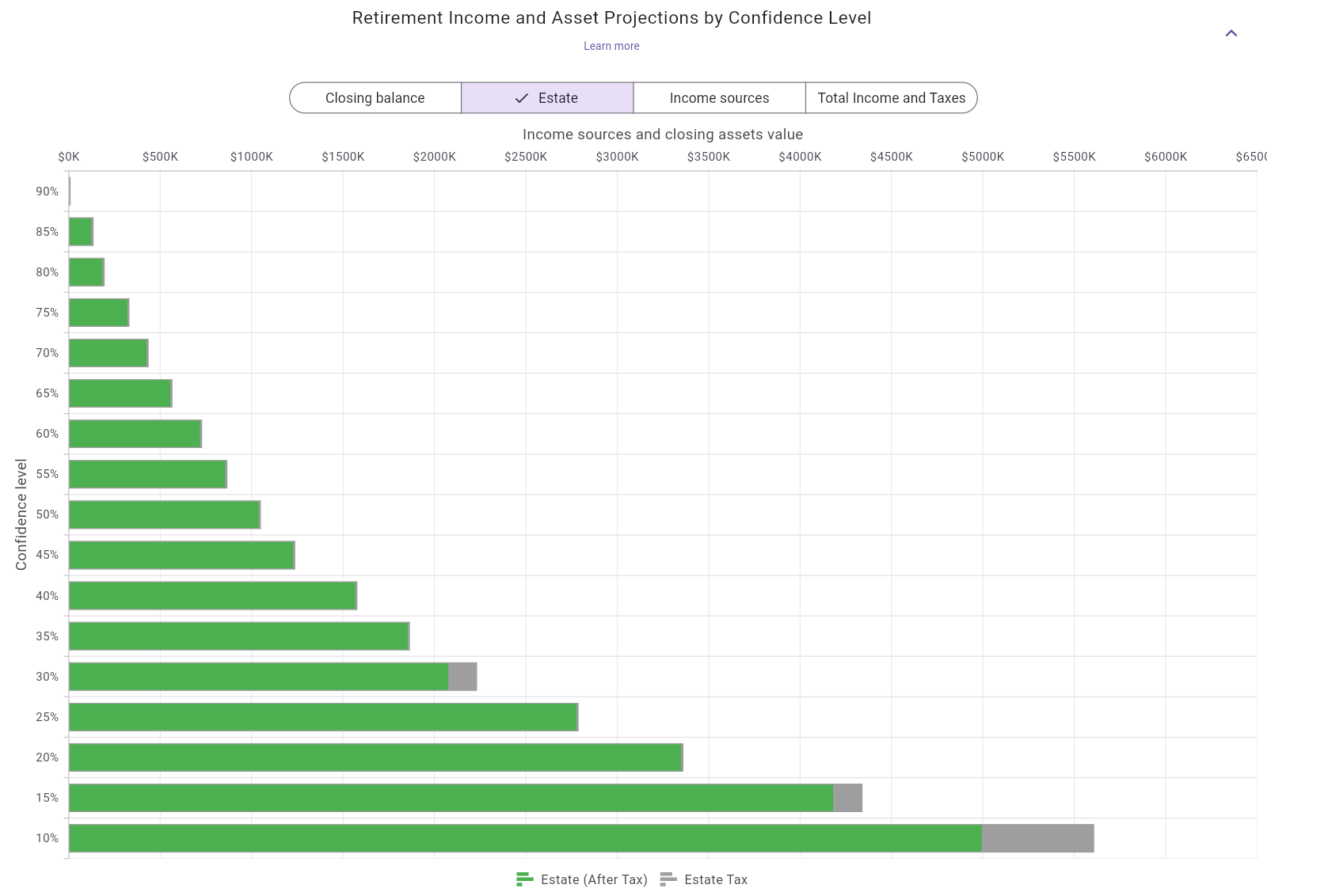

This is one chart component with multiple tabs. The two views below are different tabs of the same chart:

Closing balance tabEstate tab

Figure 83: Confidence-level chart in Closing balance tab

Figure 84: Confidence-level chart in Estate tab

What this chart shows:

Closing balance: closing asset mix by

account/category.Estate: after-tax estate and estate-tax

composition.How to read it:

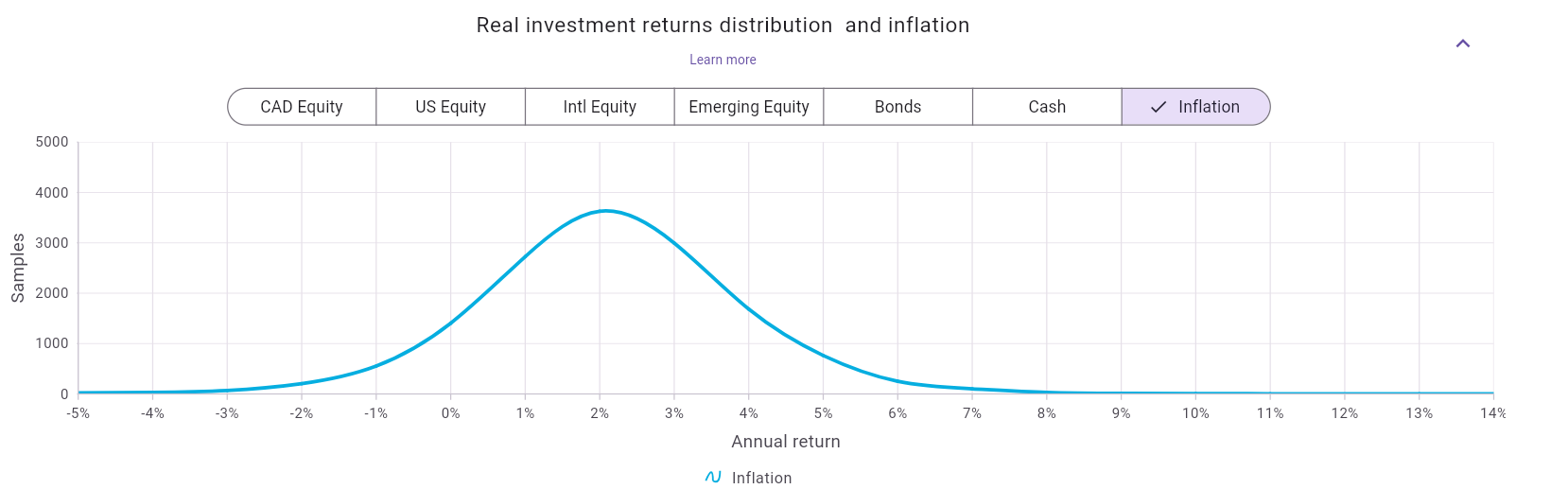

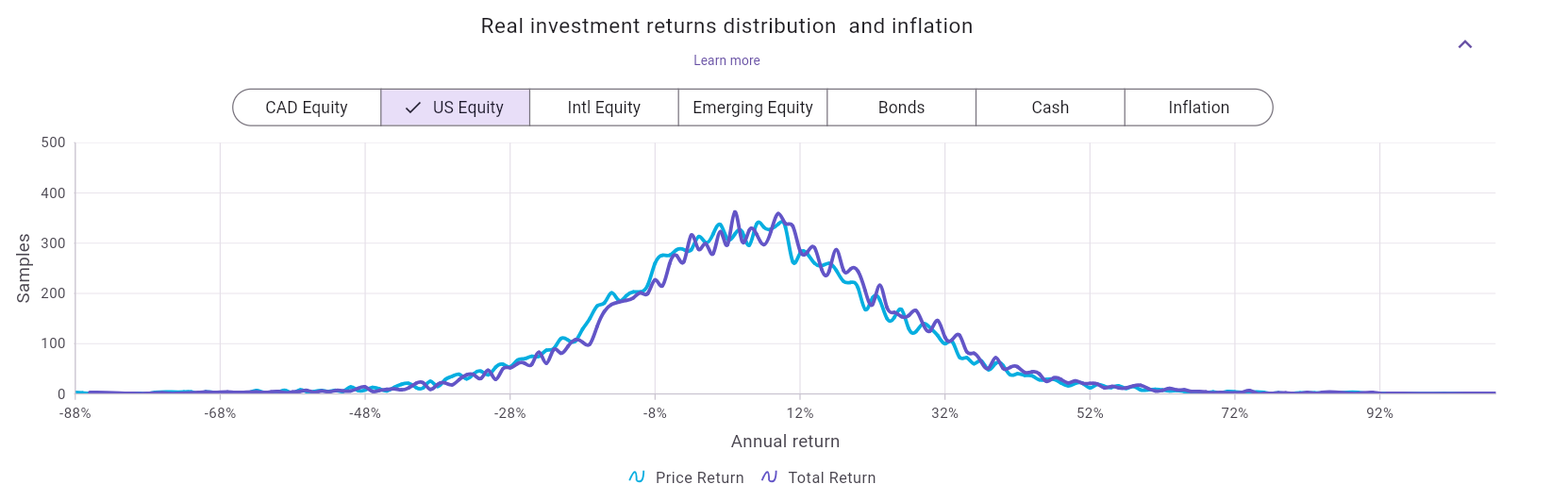

This chart is also tabbed. The examples below show:

Inflation tabUS Equity) showing return distributions

for that asset class

Figure 85: Real investment returns distribution chart - Inflation tab

Figure 86: Real investment returns distribution chart - Asset class tab example (US Equity)

What this chart shows:

Advanced modeling note (technical/internal):

Why this matters for interpretation:

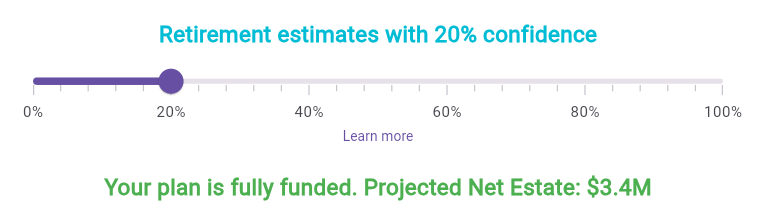

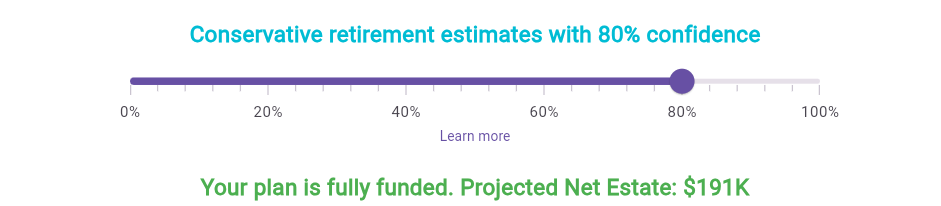

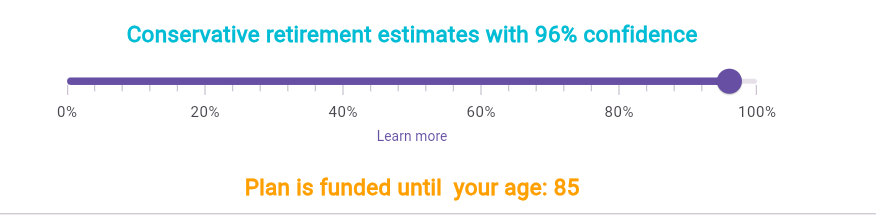

The confidence slider lets you pick a specific confidence level and immediately view one corresponding retirement outcome in the same style as Calculate (funded banner, charts, and detailed table for that selected level).

Figure 87: Confidence slider example at 20%

Figure 88: Confidence slider example at 80%

Figure 89: Confidence slider example at 96%

What “confidence level” means in this context:

How to use it:

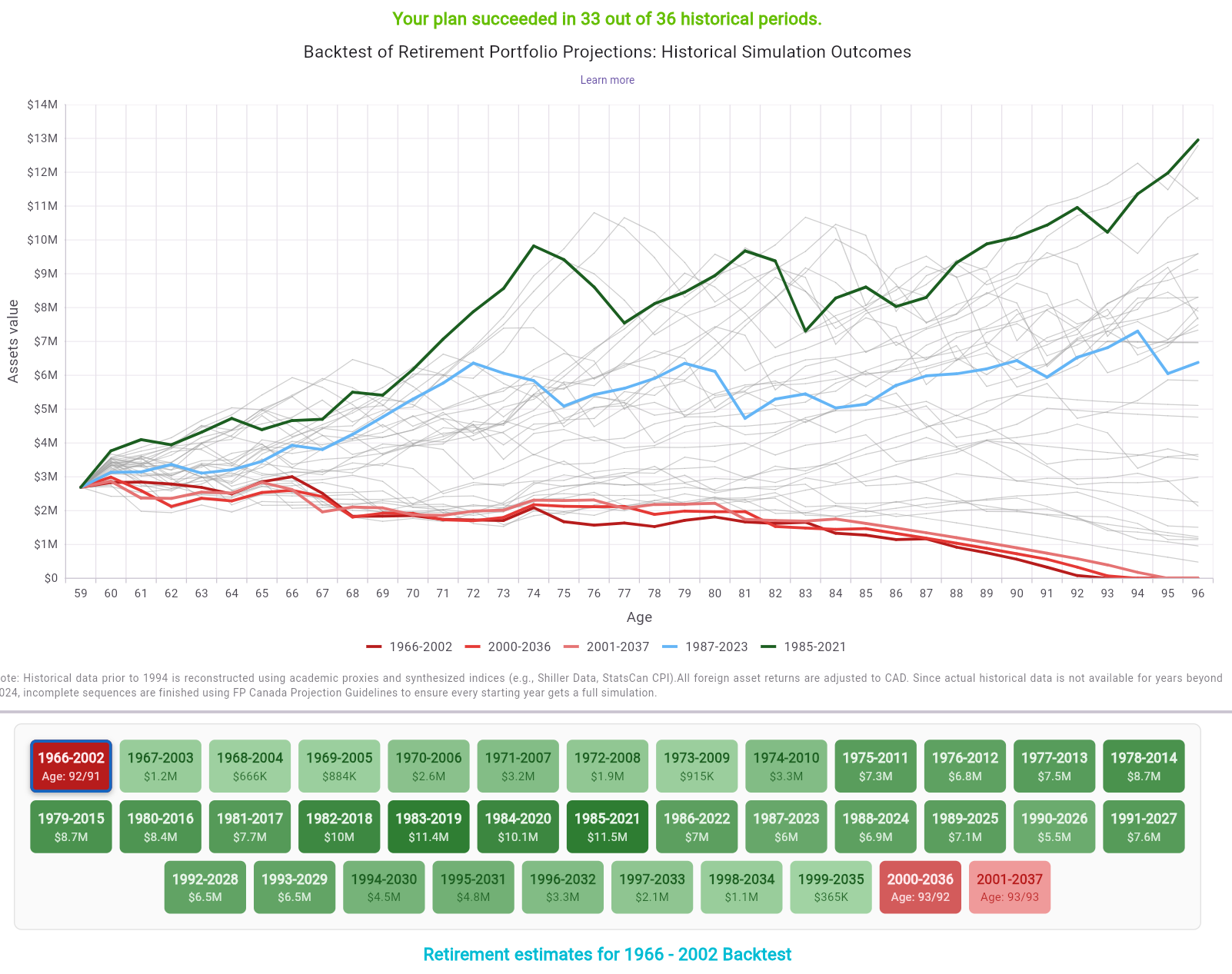

Backtesting runs your plan through many historical return windows. The backtesting screen shows all tested periods together, highlights strongest and weakest outcomes, and lets you drill into any specific period.

Figure 90: Backtesting outcomes with historical-period tiles and selected-sequence focus

What this view shows:

How to use it:

Interpretation guidance:

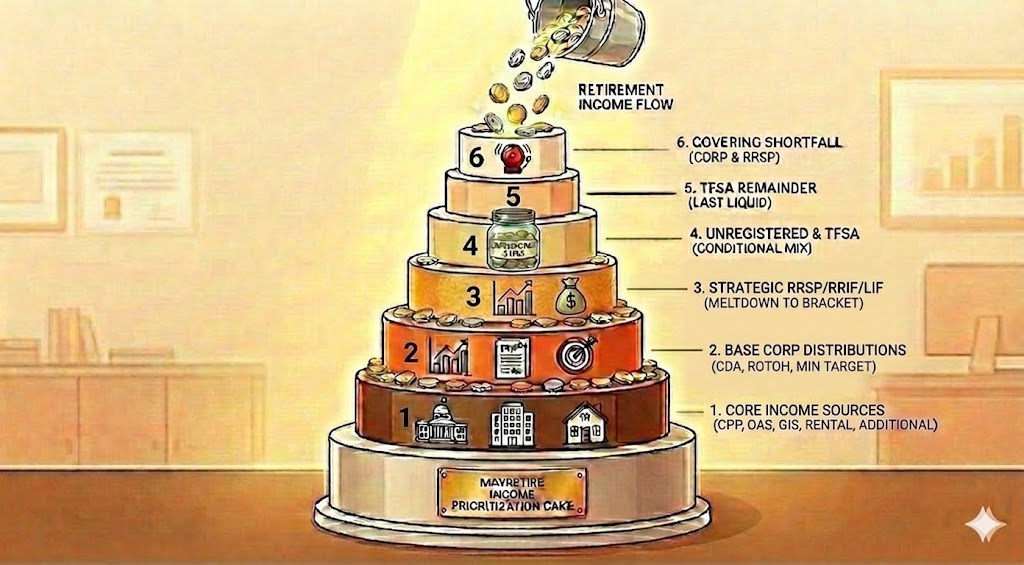

MayRetire uses a flexible withdrawal engine to meet your required retirement income while respecting your strategy settings and tax-efficiency rules.

Figure 91: Income source priority and fallback sequence

Default priority sequence:

Important interpretation note:

Thank you for reading the MayRetire tutorial.

If you have feedback, ideas, or feature suggestions, please contact

us at support@mayretire.com.

We wish you successful retirement planning with MayRetire: https://mayretire.com

Follow MayRetire for updates and tips: